Blogs

Blog title place here

We understand that every federal employee's situation is unique. Our solutions are designed to fit your specific needs.

Blog title place here

We understand that every federal employee's situation is unique. Our solutions are designed to fit your specific needs.

Blog title place here

We understand that every federal employee's situation is unique. Our solutions are designed to fit your specific needs.

A Federal Retiree's Guide to FEGLI After Retirement

Figuring out what to do with your Federal Employees' Group Life Insurance (FEGLI) is one of the most important decisions you'll make as you plan for retirement. The short answer is yes, you can keep your FEGLI coverage. But it’s not automatic. You have to make some very specific choices, and once you make them, they are permanent and irrevocable.

Understanding Your FEGLI Choices in Retirement

As you get ready to leave federal service, your FEGLI plan demands your full attention. Don't think of it as a benefit that just rolls over with you. Instead, see it as the final, critical decision for a policy you've been paying for your entire career. The choices you make will directly affect your monthly annuity payment and the death benefit your family will one day receive.

The Five-Year Rule for Eligibility

Before you can even consider your options, you have to clear one major hurdle: the "five-year rule." To carry any part of your FEGLI coverage into retirement, you must have been enrolled in that specific coverage for the five full years leading up to your retirement date.

This rule is strict and has no exceptions. If you dropped Basic FEGLI a decade ago and just picked it back up last year, you won't be eligible to keep it in retirement. You have to meet that five-year mark.

This rule applies to each part of your FEGLI coverage separately—Basic, Option A, Option B, and Option C. So, it's possible you could qualify to keep your Basic and Option C, but not your Option B if you haven't held it for the required five years.

No Increases After Retirement

Here’s another fundamental rule to lock in: you cannot increase your life insurance coverage once you retire. The amount of coverage you have on your very last day of work is the absolute maximum you can carry forward. Your retirement election is a one-time chance to decide how much of that coverage to keep or reduce, never to add more.

This is exactly why thinking through your FEGLI after retirement strategy should start years before you ever fill out your retirement paperwork.

The FEGLI program itself is massive, which speaks to its importance in long-term financial security. It’s the largest group life insurance program in the world, covering over 4 million federal employees and retirees since it began way back on August 29, 1954.

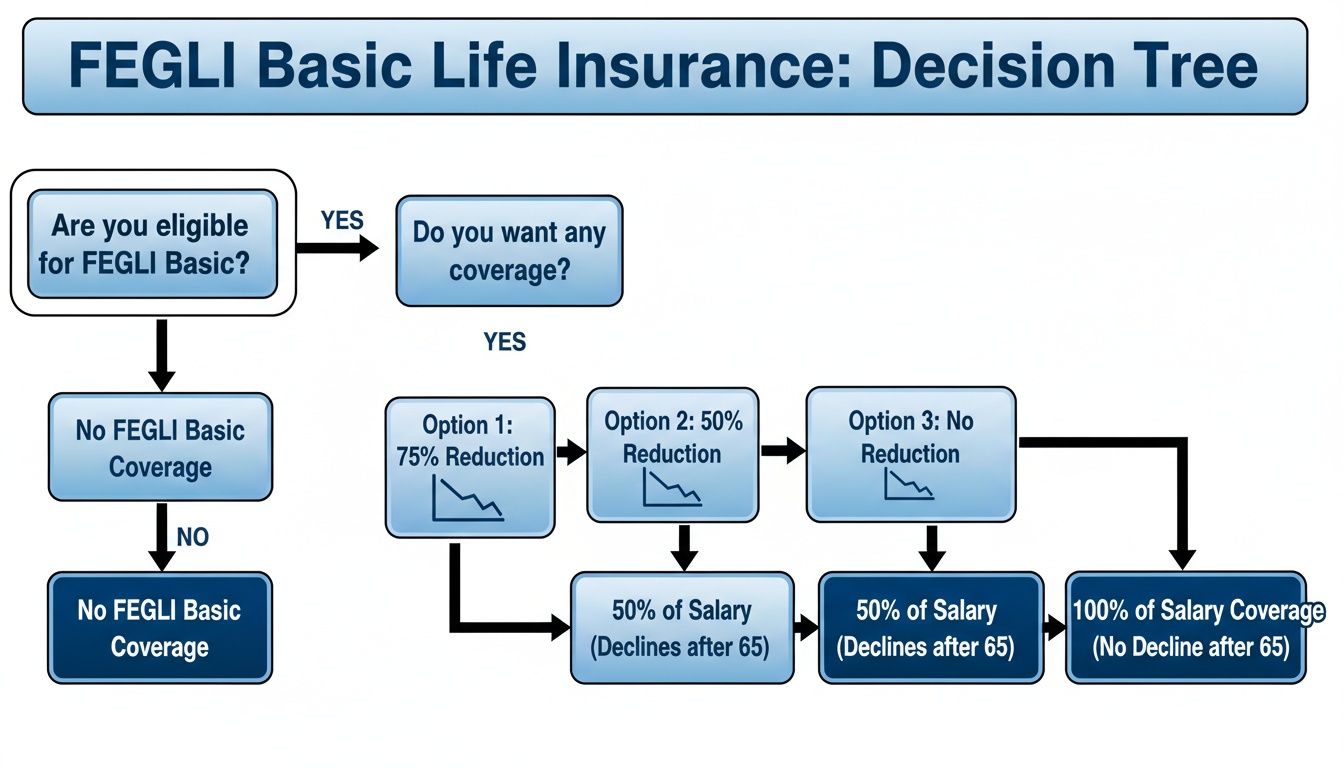

Your Three Core Choices for Basic FEGLI

At the center of your decision are three options for what happens to your Basic insurance. This is the first and biggest choice you’ll make on your retirement forms. You can find an even deeper dive in our complete guide to federal employee life insurance after retirement.

Here are your choices:

- 75% Reduction: With this option, your coverage value slowly decreases over time, but the good news is you stop paying premiums for it once you turn 65.

- 50% Reduction: Your coverage drops to half of its original value, and in exchange, you pay a lower premium for the rest of your life.

- No Reduction: You keep 100% of your Basic insurance value, but this comes at a cost—you'll pay a much higher premium for life.

Each path has very different financial outcomes, forcing you to weigh the ongoing cost against the final payout for your beneficiaries.

What Happens to Your Basic FEGLI When You Retire?

When you clock out for the last time, your Basic FEGLI coverage doesn't just disappear—but it does change. The big decision you have to make is how much of that coverage you want to keep and, just as importantly, how much you're willing to pay for it.

You're given three distinct paths, each with its own balance of cost versus benefit. Think of it like choosing a long-term plan for a valuable asset. Let's walk through each one so you can see which makes the most sense for your situation.

The 75% Reduction: The "Paid-Up" Path

This is, by far, the most popular choice among federal retirees, and for one simple reason: it eventually becomes free.

When you elect the 75% Reduction, you keep paying the same Basic insurance premium you did as an employee right up until you turn 65 (or at retirement, if you're already past that age). Then, the magic happens:

- Your premiums stop. Forever. You won't owe another penny for your Basic coverage.

- Your coverage value starts to decrease. Each month, it will reduce by 2% of its original face value until it hits just 25% of what you started with.

Let’s say you retire with $150,000 in Basic insurance. Starting at age 65, it would drop by $3,000 per month for 37.5 months. After that, your death benefit would lock in at $37,500 for the rest of your life, completely paid up. You're essentially trading a larger death benefit for a smaller one that costs you nothing in your later years.

The 50% Reduction: A Middle-of-the-Road Approach

What if you want to keep a more substantial amount of coverage without breaking the bank? The 50% Reduction option is designed to be a solid compromise.

With this choice, your coverage also begins to decrease at age 65, but more slowly. It reduces by 1% per month until it reaches half of its original value. A key difference here is that you will continue paying a premium for the rest of your life to keep it. The good news? That premium is far more manageable than the cost of keeping the full amount.

This option is a true hybrid. You accept a partial reduction in your death benefit in exchange for a reasonable lifelong premium, letting you leave behind a much larger legacy than the 75% reduction allows.

Using our same $150,000 example, the coverage would reduce by $1,500 per month until it stabilized at $75,000. You'd then pay a modest, fixed premium for life to maintain that $75,000 benefit for your beneficiaries.

No Reduction: Maximum Coverage at Maximum Cost

The No Reduction option is as straightforward as it gets. You choose to maintain 100% of your Basic FEGLI coverage for life. If you retire with $150,000 of insurance, your death benefit will remain $150,000 until the day you pass away. This is the path for providing the absolute maximum payout.

That security, however, comes with a hefty price tag. To keep the full value, you'll be on the hook for a much higher premium for the rest of your life. These payments can become a significant financial burden, especially when you're living on a fixed retirement income. This election is often best for those in poor health who can't get private insurance or for people who have a critical financial need that demands the full death benefit, no matter the cost.

FEGLI Basic Insurance Retirement Options at a Glance

Making sense of these trade-offs can be tricky. This table lays out the core differences between your three choices for your Basic FEGLI after retirement.

| Reduction Option | Premium Cost After Age 65 | Final Coverage Value | Best For Retirees Who... |

|---|---|---|---|

| 75% Reduction | $0.00 (Becomes free) | 25% of original coverage | ...want to eliminate a monthly bill and are comfortable with a smaller, permanent death benefit. |

| 50% Reduction | Moderate monthly premium | 50% of original coverage | ...want to balance a significant death benefit with a manageable, lifelong premium cost. |

| No Reduction | High monthly premium | 100% of original coverage | ...need to maximize their death benefit and can comfortably afford the much higher lifetime premiums. |

Ultimately, there's no single "right" answer. The best choice hinges entirely on your personal finances, your family's future needs, and what brings you peace of mind. Are you focused on cutting down your monthly expenses, or is leaving the largest possible inheritance your top priority? Answering that question is the first step toward making a decision you can feel good about.

Navigating Your Optional FEGLI Coverages

Once you have your Basic FEGLI plan sorted out, it's time to turn your attention to the optional layers: Option A, Option B, and Option C. Each of these operates under its own unique set of rules, so you can't just apply a one-size-fits-all strategy. Think of them as different tools in your retirement toolbox—you’ll need a specific plan for each one.

This is where we’ll get into the nitty-gritty. We'll walk through the straightforward reduction of Option A, the family-focused decisions you’ll make for Option C, and the critical cost-benefit analysis needed for the often-hefty Option B.

This decision tree gives you a great visual for how to think about your FEGLI Basic coverage, which is the foundation all these optional choices are built on.

As you can see, each reduction path—whether you pick 75%, 50%, or No Reduction—leads to a very different outcome for both your monthly premiums and the final death benefit your loved ones will receive.

Option A Standard Insurance

Let's start with the easy one: Option A. This is a flat $10,000 of extra coverage. If you’re eligible to carry it into retirement, its path is already set for you, so there are no tough choices to make here.

Option A is designed to become "paid-up" over time, much like the 75% Reduction choice for your Basic coverage. You’ll continue paying the premiums for it until you turn 65 (or at the moment you retire, if you're already past that age).

Once you hit that 65-year milestone, a couple of things happen automatically:

- The premiums disappear. That's right, you'll never pay another dime for Option A.

- The benefit starts to reduce. Your $10,000 of coverage will shrink by 2% each month ($200) until it bottoms out at $2,500.

This process takes 37.5 months, and after that, the $2,500 death benefit is locked in for the rest of your life, completely free of charge.

Option C Family Coverage

Option C is what provides life insurance for your spouse and any eligible children, and unlike Option A, it gives you some real decisions to make in retirement. First off, you have to decide if you even want to keep it.

If you do, you then have to choose how many "multiples" to hang on to—anywhere from one to five. Each multiple is worth $5,000 of coverage for your spouse and $2,500 for each eligible child.

A critical point to remember here is that you'll pay premiums for Option C for the rest of your life, and they get more expensive as you get older. The cost is based on your age, not your spouse's, with the price jumping up every five years. This means you have to constantly ask yourself if the cost is still worth the benefit.

You’ll also have to choose between a "Full Reduction" or "No Reduction" for your coverage after you turn 65. If you pick Full Reduction, the coverage becomes free at 65, but it will decrease by 2% per month until it’s completely gone. If you pick No Reduction, you keep paying those escalating premiums to maintain the full coverage amount. Our guide on a complete guide to federal life insurance fegli dives even deeper into these choices.

The Critical Decisions for Option B

And now we come to Option B. For many federal employees, this is the biggest, most expensive, and most complicated piece of the entire FEGLI puzzle. The coverage amount can be massive—up to five times your salary—which offers a lot of protection but also comes with a serious price tag.

Unlike your Basic insurance, you pay the full cost for Option B, and the premiums spike dramatically every five years. It's manageable when you're younger, but the costs can become astronomical in retirement.

When you retire, you have two major decisions to make for Option B:

- How many multiples to keep: Just like Option C, you can keep anywhere from one to all five of your multiples.

- Whether to elect Full Reduction or No Reduction: This is, by far, the most important decision you will make regarding your FEGLI benefits.

With No Reduction, you keep the full death benefit, but you are signing up to pay premiums that will skyrocket for the rest of your life. It’s not an exaggeration to say that for many retirees, these premiums can eventually grow to be more than their entire monthly pension payment.

The other path is Full Reduction. If you choose this, your Option B coverage becomes free once you turn 65. The catch? Starting at age 65, the coverage value drops by 2% per month for 50 months until it hits zero and disappears completely.

This leaves you with a very tough choice: pay a fortune to keep your coverage, or let it vanish for free. For many people, the best answer isn't on the official form at all. It's canceling Option B and finding a private life insurance policy that offers more stability and long-term value for their money.

Comparing FEGLI Costs to Private Insurance

Deciding what to do with your FEGLI after retirement often comes down to one simple question: is it the best value for your money? The convenience of just rolling over your group plan is certainly tempting, but it might not be the most cost-effective way to protect your family’s future. To really know, you have to put FEGLI in a head-to-head comparison with private insurance, especially when we're talking about the notoriously expensive Option B.

This isn't about finding a single "right" answer for everyone—your situation is unique. It's about giving you the tools to run the numbers for yourself and see if a private policy could offer better, or at least more predictable, financial protection for your loved ones.

The FEGLI Ace in the Hole: The Medical Exam

Before we get into the dollars and cents, let’s talk about FEGLI's single biggest advantage: no medical exam is required to keep your coverage when you retire. If you have significant health conditions that would make it difficult or impossible to get a policy on the private market, keeping FEGLI might be your only realistic choice.

This is a powerful benefit, and for anyone in poor health, the higher cost of FEGLI can be a necessary trade-off to make sure their family is taken care of. However, if you're in reasonably good health, this advantage effectively vanishes. That's when the door swings wide open to potentially much cheaper private alternatives.

A Tale of Two Policies: FEGLI Option B vs. Private Term Life

Let's walk through an example. We'll call our federal employee "David." He's retiring at age 60, is a non-smoker in good health, and currently has $300,000 of FEGLI Option B coverage (that’s two multiples of his $150,000 salary). His goal is to make sure his spouse is financially secure until they both reach age 80.

Here’s a look at how his costs could play out:

FEGLI Option B Premiums: At age 60, his monthly premium for that $300,000 of coverage is $222.30. By the time he hits age 70, the exact same coverage will cost him $780.00 a month. If he makes it to age 80, the monthly premium balloons to an incredible $1,890.00.

Private 20-Year Term Policy: David shops around and gets a quote for a $300,000, 20-year term life insurance policy. Since he's in good health, his premium is locked in at around $180 per month for the entire 20 years.

Right out of the gate, David saves over $40 a month. But the real savings pile up over time. By his 70s, he’s saving nearly $600 a month compared to what he would have paid for FEGLI. That kind of stability from a fixed premium is a huge relief when you’re living on a fixed retirement income.

The escalating, age-banded premium structure of FEGLI Option B is its greatest weakness. What starts as a reasonable cost can quickly become an unsustainable drain on your monthly annuity, forcing many retirees to drop coverage when they may need it most.

Key Factors in Your Personal Comparison

David's story is just one scenario. To make a smart decision for yourself, you need to weigh a few key factors honestly.

1. Your Current Health This is the big one. Can you pass a medical exam for a private policy? If the answer is no, then FEGLI's guaranteed coverage is invaluable, plain and simple.

2. Your Family's Actual Needs Think about how much coverage you truly need and for how long. Are you trying to replace your income for 10 years, 20 years, or the rest of your life? A private term policy can be tailored to a specific timeframe, like paying off a 15-year mortgage, which often makes it a much more efficient tool.

3. Long-Term Cost Trajectory Don't get fixated on today's premiums. You need to project the costs for both FEGLI and a private policy over the next 10, 15, and 20 years. This long-range view is what usually exposes the staggering financial difference. Beyond just insurance, this decision is part of a bigger plan to create a resilient retirement income stream that can withstand these kinds of rising costs and keep your overall financial life healthy.

How to Lock In Your Final FEGLI Choices

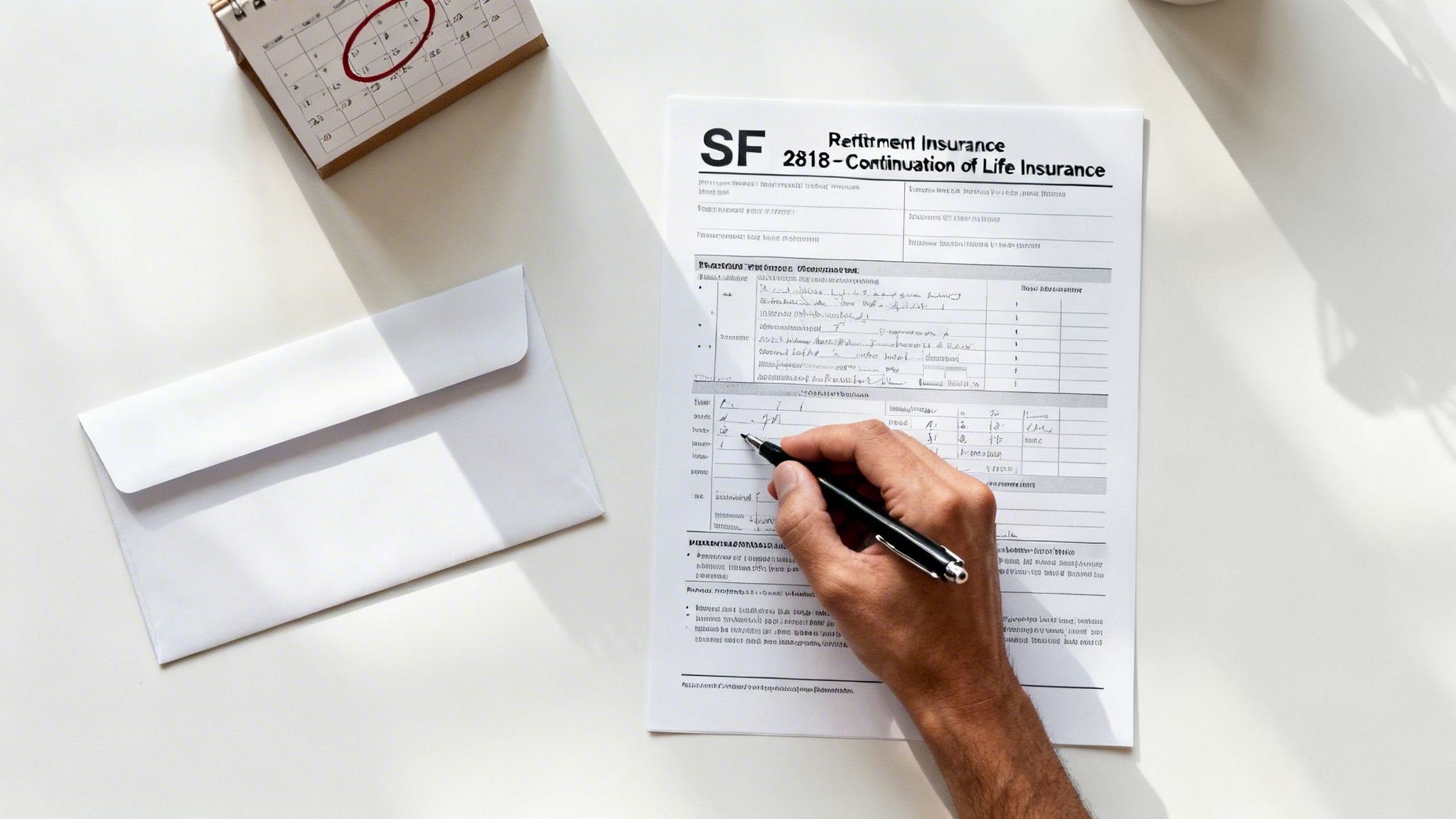

After you've weighed all the pros and cons of your FEGLI after retirement options, it’s time to make your final call. This isn't just another form to fill out—it's a legally binding decision that will stick with you for the rest of your life. Getting it right is crucial.

The key to this whole process is a single document: the SF 2818, Continuation of Life Insurance Coverage. Think of this form as your final instruction manual for OPM. It's submitted along with your retirement application, and it tells the government exactly what you want to do with your life insurance.

Getting the SF 2818 Form Right

The SF 2818 is where you spell out your wishes for each piece of your FEGLI coverage—Basic, Option A, Option B, and Option C. You have to be crystal clear.

For your Basic Insurance, you’ll see three boxes. You must check one:

- 75% Reduction

- 50% Reduction

- No Reduction

Pick one, and only one. If you leave it blank or check multiple boxes, you risk serious delays, and OPM will likely default you into the 75% Reduction, whether you wanted it or not.

For your Optional coverages, you’ll do something similar. You'll state which ones you’re keeping and, for Options B and C, decide if you want the "No Reduction" feature. Be sure to write down the exact number of multiples you plan to continue.

Common Pitfalls to Sidestep

A simple mistake on this form can have expensive consequences. I’ve seen countless federal employees accidentally lock themselves into choices they didn’t want, leading to sky-high premiums or lost coverage.

The most common error I see is with the "No Reduction" boxes. If you want your coverage to reduce over time (and become free or cheaper), you leave the "No Reduction" box unchecked. Checking it means you're signing up for lifelong premiums to keep the full amount.

Here are a few other mistakes that pop up all the time:

- Forgetting to Sign and Date: An unsigned form is a dead end. OPM will send it back, and your entire retirement process will stall.

- Sloppy Handwriting: If they can't read it, they can't process it. It’s that simple. Print everything clearly.

- Missing the Deadline: The SF 2818 goes in with your retirement application. There’s no grace period to change things once your retirement is finalized.

Understanding how to fill out these forms correctly is a skill you build throughout your career. You can learn more about managing your benefits in our essential FEGLI enrollment guide for active employees.

This Decision is Final—And We Mean Final

I can't say this enough: the choices you make on the SF 2818 are irrevocable. Once OPM finalizes your retirement, there are no do-overs. You can't switch from a 75% Reduction to a 50% Reduction later, and you can't add back Option B multiples you decided to let go.

The only change you can make down the road is to reduce or cancel coverage. For example, you can always decide to stop paying for "No Reduction" coverage, but you can never get it back once you do. This is a one-way street.

So, triple-check your form before you submit it. Better yet, have a trusted spouse or advisor look it over with you. Make a copy for your personal records and rest easy knowing you've secured your financial legacy exactly the way you planned.

Common Questions About FEGLI in Retirement

Once you've made your big decisions about FEGLI for retirement, the smaller, more specific questions often start to pop up. Let's tackle some of the most common ones that federal retirees ask.

Can I Change My FEGLI Reduction Choice After I Retire?

In a word, no. The choice you make on your SF 2818 form about how your Basic and Optional insurance will reduce is a done deal once the Office of Personnel Management (OPM) finalizes your retirement. You can't, for example, decide a few years in that you'd rather have the 50% Reduction instead of the 75% Reduction.

This is why that initial decision is so important. Once it's made, it's considered irrevocable. The only change you can make later is to cancel your coverage completely. You can never increase it or switch to a different reduction schedule.

Think of your retirement election as a permanent, one-time decision. Once that choice is locked in, your only options are to keep the coverage as is or cancel it entirely. There are no do-overs down the road.

What Happens to My FEGLI if I Leave Federal Service Before Retirement?

This is a critical point: keeping your FEGLI coverage is a benefit tied directly to being eligible for an immediate retirement annuity. If you leave your federal job before you can draw an immediate pension, you can't keep your group life insurance.

But you won't be left completely high and dry. You'll be given a 31-day window to convert your FEGLI coverage into an individual private policy.

Here’s what you need to know about this conversion option:

- No Medical Exam Required: The biggest advantage is that you can get the policy without having to prove you're insurable. This is a huge benefit if you have health issues.

- Premiums Will Be Much Higher: Be prepared for sticker shock. The new policy will be based on commercial rates for an individual, which are significantly more expensive than the group rates you were used to as a federal employee.

Do I Have to Keep All Parts of My FEGLI Coverage?

Not at all. You don't have to treat FEGLI as an all-or-nothing package. You have the flexibility to cancel certain parts of your coverage while keeping others.

For instance, a popular strategy for many retirees is to drop the increasingly expensive Option B coverage as they get older, but hang on to their Basic and Option C (family) policies. You can cancel any portion of your FEGLI at any time after you retire simply by sending a signed letter to OPM. Just remember, any cancellation is permanent—you can't get it back later.

At Federal Benefits Sherpa, we help you get clear answers to these critical questions before you make a decision you can't undo. Schedule a free consultation to make sure your FEGLI strategy is a perfect fit for your retirement goals. You can learn more at https://www.federalbenefitssherpa.com.

Dedicated to helping Federal employees nationwide.

“Sherpa” - Someone who guides others through complex challenges, helping them navigate difficult decisions and achieve their goals, much like a trusted advisor in the business world.

Email: [email protected]

Phone: (833) 753-1825

© 2024 Federalbenefitssherpa. All rights reserved