What Is FERS Retirement Supplement? what is fers retirement supplement

If you’re a federal employee planning to retire before age 62, you’ve probably heard whispers about the FERS Special Retirement Supplement, or SRS. What exactly is it? Think of it as a financial bridge, designed specifically to help you cross the gap between your retirement date and the day you can finally claim Social Security.

This supplement acts as a stand-in for the Social Security benefits you earned during your years of FERS civilian service. It makes retiring early a much more realistic option for many long-serving feds. But there's a catch: the supplement stops cold the month you turn 62, whether you decide to start your actual Social Security checks then or not.

The Financial Bridge to Your Full Retirement

The Federal Employees Retirement System (FERS) was built from the ground up knowing that many dedicated employees would want to retire with a full career under their belt, even if they weren't old enough for Social Security. The SRS is the key provision that makes this possible.

Why Does the Supplement Exist?

At its core, the supplement exists to provide an income stream that closely mimics the Social Security payment you've earned from your FERS-covered work. It’s a way to ensure that you aren't left with a major income shortfall while you wait for your Social Security eligibility to kick in.

The FERS system itself is famously known as a three-legged stool, with each leg representing a different source of retirement income:

- The FERS Basic Annuity: This is your main pension payment, the reward for your years of service.

- The Thrift Savings Plan (TSP): Your 401(k)-style investment account that you've hopefully been contributing to throughout your career.

- Social Security: The federal benefits program you've been paying into your entire working life.

The SRS essentially acts as a temporary prop for that third leg—Social Security—until it's strong enough to stand on its own at age 62.

Key Takeaway: The FERS supplement isn't some kind of extra bonus. It's a calculated, temporary payment managed by the Office of Personnel Management (OPM). It stops automatically when you hit age 62, making this date a critical milestone in your retirement plan.

To give you a clearer picture, here is a quick overview of what the SRS is all about.

FERS Special Retirement Supplement (SRS) at a Glance

| Component | Key Details |

|---|---|

| Purpose | To "bridge the gap" between early FERS retirement and Social Security eligibility (age 62). |

| Source | Paid by the Office of Personnel Management (OPM), not the Social Security Administration (SSA). |

| Eligibility | Must be eligible for an immediate, unreduced FERS retirement. |

| Payment Window | Starts at your Minimum Retirement Age (MRA) and ends automatically the month you turn 62. |

| Calculation | An estimate of the Social Security benefit earned during your FERS service years. |

| Earnings Test | Subject to the same earnings limit as Social Security recipients under their full retirement age. |

This table provides a high-level look, but understanding the details is crucial for anyone considering retiring from federal service before age 62. This guide will walk you through everything you need to know, from who qualifies to how the numbers are crunched, because the SRS directly impacts your budget and financial stability during those first few exciting—and vital—years of retirement.

Confirming Your Eligibility for the FERS Supplement

So, will you get the FERS Special Retirement Supplement (SRS)? That's a critical question, and the answer isn't a simple "yes" for everyone. It's crucial to understand that not every federal retiree qualifies, and the rules are quite specific.

Think of the supplement as a bridge payment, designed specifically for long-serving Feds who decide to retire before they can start drawing Social Security. The eligibility rules are built around this one core idea: rewarding a full career.

The Standard Pathways to Eligibility

For most federal employees, qualifying for the FERS supplement boils down to meeting certain age and service milestones for an immediate, unreduced retirement. There are really two main paths.

You're on track to receive the supplement if you retire:

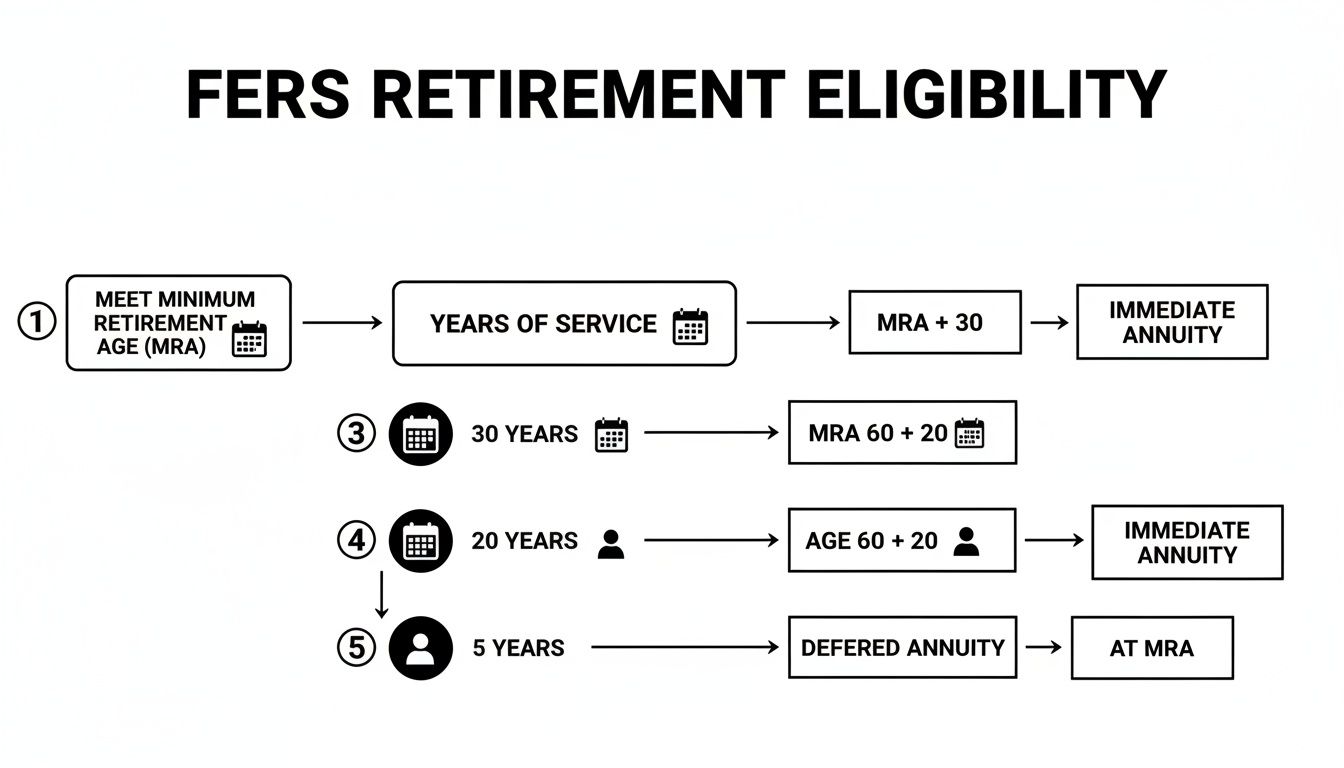

- At your Minimum Retirement Age (MRA) with at least 30 years of creditable service. Depending on when you were born, your MRA falls somewhere between age 55 and 57.

- At age 60 with at least 20 years of creditable service. This route is great for those who might have started their federal careers a little later but still put in two solid decades.

Here's a key detail that trips people up: the service years must be creditable FERS service. You can absolutely buy back military time to help you become eligible to retire and to increase your FERS pension, but those military years do not count toward calculating the amount of your supplement.

If you need a refresher on these rules, you can learn more about FERS retirement eligibility in our detailed guide.

Special Provisions for Early or Involuntary Retirement

What happens if you don't fit into those two neat boxes? Life happens, and sometimes retirement comes unexpectedly. The Office of Personnel Management (OPM) has special rules for situations like agency buyouts or involuntary separations.

You might still be eligible for the supplement under these conditions:

- Voluntary Early Retirement Authority (VERA): If your agency offers a "VERA" and you take it, you can retire at age 50 with 20 years of service, or at any age with 25 years of service, and still get the supplement.

- Involuntary Retirement: If you're forced out through no fault of your own—like during a Reduction in Force (RIF)—you can also qualify for the supplement if you meet the same VERA criteria (50/20 or any age/25).

A Critical Reminder: The FERS supplement is a temporary benefit. No matter how you qualify or when you start receiving it, the payments stop permanently the month you turn 62. That deadline is set in stone.

This benefit was part of the FERS package from the very beginning, back in 1987. It was always intended to support those who put in a full career but chose to retire early. Understanding which of these pathways you fall into is the first step in figuring out if this financial bridge will be part of your retirement plan.

How to Estimate Your FERS Supplement Payout

Trying to figure out your FERS Special Retirement Supplement (SRS) can feel like a chore, but the official OPM formula is surprisingly straightforward once you peel back the government-speak. Let's walk through it together.

To make this real, we'll follow a hypothetical federal employee named "Federal Frank." His example will show you exactly how the pieces fit, giving you the confidence to run your own numbers.

Step 1: Find Your Estimated Social Security Benefit

First things first, you need to find out what your Social Security benefit is estimated to be at age 62. This number is the foundation of the entire calculation, so getting it right is key.

The most reliable place to find this is on your official Social Security statement. You can get yours by setting up a free account on the Social Security Administration's website. Once you're in, look for the estimated monthly benefit at age 62.

Let's say Frank logs in and sees his estimated Social Security benefit at age 62 will be $2,000 per month. We’ll use that as our starting point.

Step 2: Tally Your Years of FERS Service

Next, add up your total years of creditable FERS civilian service. This is simply the number of years you’ve worked under the FERS system.

One common trip-up here is military time. While buying back your military service is great for your FERS annuity and helps you hit your retirement eligibility date, those years do not count toward the supplement. Only civilian time matters for this formula.

In our example, Federal Frank has put in 30 years of civilian federal service.

Step 3: Apply the Simple Formula

With those two numbers in hand, we can plug them into the SRS formula. It’s much simpler than most people expect.

Here’s the basic structure:

(Your Years of FERS Service / 40) x Your Estimated Social Security Benefit at 62 = Your Estimated Monthly Supplement

Let’s run the numbers for Frank:

- Years of FERS Service: 30

- Estimated Social Security at 62: $2,000

The calculation is: (30 / 40) x $2,000 = $1,500

So, Frank’s estimated monthly FERS supplement would be $1,500. He’d receive this payment on top of his regular FERS pension every month from his retirement date until he turns 62.

Why the number 40? The formula uses 40 as a stand-in for a full working career, roughly from age 22 to 62. It’s a simple benchmark to compare your FERS service against.

Here’s a step-by-step table to make it even clearer.

Example FERS Supplement Calculation Walkthrough

| Step | Action | Example Value ('Federal Frank') | Calculation |

|---|---|---|---|

| 1 | Find Estimated Social Security Benefit at Age 62 | $2,000 per month | N/A |

| 2 | Count Total FERS Civilian Service Years | 30 years | N/A |

| 3 | Divide FERS Service by 40 | 30 years | 30 / 40 = 0.75 |

| 4 | Multiply Result by Estimated Social Security Benefit | 0.75 | 0.75 x $2,000 |

| 5 | Final Estimated Monthly Supplement | $1,500 | $1,500 |

This walkthrough shows just how manageable the calculation can be when you break it down into simple steps.

The infographic below shows the main retirement paths that make you eligible for the supplement in the first place.

As you can see, the two main routes to qualify are retiring at your Minimum Retirement Age (MRA) with 30 years of service or at age 60 with 20 years.

What About Partial Years of Service?

A great question I get all the time is how partial years are handled. Thankfully, OPM doesn’t just round down; they calculate your service down to the month.

For instance, if you worked for 25 years and 6 months, your service credit for the formula would be 25.5 years. This makes sure you get credit for every single month you’ve worked.

This benefit is a big deal. The FERS Special Retirement Supplement impacts retirement timing for over 500,000 annuitants, and the payouts often land between $500-$800 a month for those with 25 to 35-year careers.

While running these numbers yourself gives you a solid estimate, it's always good to use a dedicated tool. To model different scenarios, I recommend checking out our guide on finding the best retirement calculator for FERS employees. It will help you see how the supplement fits into your complete retirement picture.

Be Careful: The FERS Supplement Has an Earnings Test

This is one of the most important—and most often missed—details about the FERS supplement: it isn't guaranteed income. Many early federal retirees are blindsided when they discover their supplement payment can shrink, or even vanish completely, if they earn too much from a post-retirement job. This is all thanks to the FERS Supplement Earnings Test.

Think of this test as a copycat of the rule Social Security uses for people who claim their benefits before their full retirement age. In a nutshell, if you retire from federal service before you hit 62 and then decide to work elsewhere, what you earn could take a bite out of your supplement.

How the Reduction Formula Works

The rule itself is straightforward, but the financial impact can be huge. Your FERS supplement gets docked by $1 for every $2 you earn above the annual limit. The Social Security Administration sets this limit, and it usually gets a little bump each year for inflation, so it's something you'll want to keep an eye on.

What counts as "earnings"? We're talking about wages from a job or your net earnings if you're self-employed. Good news, though: this test completely ignores other income streams like your FERS annuity payments, TSP withdrawals, investment returns, or other pensions.

Key Takeaway: The earnings test is only in effect while you're actually receiving the supplement—from the day you retire until your 62nd birthday. Once the supplement stops, this rule no longer has any bearing on your FERS benefits.

Let's See It in Action: Federal Frank's Consulting Gig

Remember our retiree, "Federal Frank"? We figured his FERS supplement would be around $1,500 a month, which works out to $18,000 for the year. Frank isn't the type to sit still, so he picks up a part-time consulting gig after retiring.

Here’s how the earnings test throws a wrench in his plans.

- The Annual Earnings Limit: For this example, let's say the limit is $22,320.

- Frank's Consulting Income: He has a good year and earns $32,320.

First, we need to see how much he went over the limit:

$32,320 (Frank's Earnings) - $22,320 (The Limit) = $10,000 (Amount Over Limit)

Now, we apply that $1-for-$2 reduction:

$10,000 / 2 = $5,000 (Total Annual Reduction)

This means Frank’s annual supplement of $18,000 gets slashed by $5,000. His new, reduced supplement is just $13,000 a year, which breaks down to about $1,083 per month. That's a far cry from the $1,500 he was expecting.

Each May, the Office of Personnel Management (OPM) sends out a survey asking what you earned in the previous year. Based on your answers, they’ll apply any reductions starting with your July payment.

Some Retirees Are Exempt From the Earnings Test

Now for some good news. Not everyone has to worry about this test. A select group of federal retirees is completely exempt, which is a massive advantage for their retirement income planning.

The earnings test does not apply if you are one of the following:

- Special Category Employees: This group includes federal law enforcement officers, firefighters, and air traffic controllers who retire under their special, earlier retirement provisions.

- Military Reserve Technicians: Specifically, those who lose their military status at age 50 and qualify for an immediate annuity are also exempt.

These folks can go out and earn as much as they want in the private sector without losing a single penny of their FERS supplement. The exemption is a recognition of the demanding nature of their careers and their earlier mandatory retirement ages. If you're trying to figure out where you stand, our guide explaining the Social Security supplement for federal employees can provide more clarity.

For everyone else, being strategic about post-retirement work is absolutely critical if you want to avoid a nasty financial surprise. Understanding this rule is fundamental to a smooth and successful early retirement.

Planning Your Financial Transition at Age 62

The FERS Special Retirement Supplement (SRS) is a temporary benefit with a hard stop. The very month you turn 62, those payments end. For federal retirees who aren't prepared, this can feel like a financial trapdoor opening up, creating a sudden and jarring income gap in their budget.

But this transition doesn't have to be a crisis. It's a built-in feature of the FERS system. The supplement, paid out by the Office of Personnel Management (OPM), was always designed to be a bridge, ending at the exact moment you first become eligible to claim Social Security. This timing forces one of the most important decisions you'll make in your early retirement years.

The Big Decision at Age 62

Once your FERS supplement disappears, you’re at a crossroads: do you start taking Social Security right away, or do you wait? There’s no one-size-fits-all answer here. The best move for you depends on your personal finances, your health, and what you want your retirement to look like long-term.

Here’s the fundamental trade-off:

- Claiming at 62: You can instantly plug the hole left by the supplement with your new Social Security check. The downside? You’re locking in a permanently reduced benefit—for the rest of your life.

- Waiting to Claim: If you have other assets to live on, you can delay claiming Social Security. Your future monthly benefit will grow substantially for every year you wait, all the way up to age 70. This strategy can secure a much larger, inflation-protected income stream later on, but it requires a solid plan to cover your expenses in the meantime.

Making this call means taking a hard look at your complete financial picture—your FERS pension, TSP savings, and any other investments you have.

Building Your Financial Bridge

It’s helpful to think of the FERS supplement as a bridge, but it’s even more critical to plan for what’s on the other side. The goal is to build a smooth financial pathway from the supplement to your permanent Social Security income, no matter when you decide to start it.

For many federal retirees, this means creating their own "bridge fund." This often involves carefully structuring withdrawals from the TSP to fill that income gap for a few years, giving your Social Security benefit time to grow into a much larger monthly payment. This is a classic FERS planning scenario, driven by the fact that the supplement stops at 62 even though claiming Social Security that early results in a benefit that's only 70-75% of your full amount.

Strategic Planning is Non-Negotiable: The end of the supplement isn't a surprise—it's a certainty. The key to a stable and stress-free retirement is deciding in advance how you will replace that income, whether it's with Social Security, your TSP, or other savings.

Integrating Health Insurance into Your Plan

Another crucial piece of the age-62 puzzle is healthcare. Remember, you won't be eligible for Medicare until you turn 65. That means you’ll be relying on your Federal Employees Health Benefits (FEHB), and those premium costs need to be a line item in your budget. This is especially true if you delay Social Security and need to pull more from your TSP to cover living expenses.

If you’re mapping out your budget, this guide on health insurance options for retiring at 62 offers some great insights for navigating the years before Medicare kicks in.

Ultimately, by treating the end of the FERS supplement not as an unexpected problem but as a planned transition point, you can build a resilient income strategy that supports you throughout your entire retirement journey.

Frequently Asked Questions About the FERS Supplement

Working through the fine print of federal benefits can feel like a puzzle, but getting a handle on the FERS Special Retirement Supplement (SRS) is a huge piece of planning a successful early retirement. To make sure you’ve got all the pieces in place, let's tackle some of the most common questions we hear from federal employees.

These quick, clear answers will help solidify what we've covered and steer you clear of some common pitfalls on the road to retirement.

Do I Need to Apply for the FERS Supplement Separately?

This question comes up all the time, and thankfully, the answer is simple: no, you do not need to file a separate application. The process is designed to be automatic for those who qualify.

When you fill out your application for an immediate FERS retirement, the Office of Personnel Management (OPM) takes it from there. As long as you meet the age and service rules for the SRS, OPM calculates the amount and bundles it right in with your monthly FERS pension payment. It's not a separate check—it just becomes part of your total deposit until you hit age 62.

Does Military Service Count for the Supplement Calculation?

Your military service is a critical part of your career, but it plays a very specific role in your federal retirement. While buying back your military time is a smart move for boosting your FERS pension and qualifying for retirement sooner, those years of service do not count toward the supplement itself.

The FERS supplement formula is based only on your years of FERS civilian service. This is a crucial detail for getting your supplement estimate right and avoiding any surprises in your retirement income.

What Happens If I Go Back to Work for the Federal Government?

Thinking about a "return to service" after retiring? You'll want to pay close attention here. If you are rehired into a FERS-covered position, both your FERS pension and your SRS payments will come to a halt for as long as you're reemployed.

This rule exists because you can't draw a federal salary and a federal retirement benefit at the same time. Your benefits can often be restarted once you separate from service again, but the rules around reemployment and how your benefits are recalculated can get tricky. It all depends on the specifics of your new job, so getting some expert advice before you make that leap is a must.

Planning for these nuances is exactly where expert guidance makes a difference. At Federal Benefits Sherpa, we help federal employees demystify their benefits to build a secure and confident retirement. To ensure your plan is on the right track, schedule your free 15-minute benefit review with us today at https://www.federalbenefitssherpa.com.