What Is a Beneficiary Designation Form and Why It Matters

A beneficiary designation form is a simple, legally recognized document that tells a financial institution exactly who gets the money in an account when you pass away. Think of it as a direct instruction manual for your Thrift Savings Plan (TSP), life insurance, or other retirement accounts. It’s a powerful tool that puts you in the driver's seat, making sure your hard-earned assets go straight to the people you choose.

What Is a Beneficiary Designation Form

You’ve worked hard to build your retirement savings and protect your family with life insurance. But how do you make sure that money gets to them without headaches or delays? That’s the job of the beneficiary designation form.

This document is essentially a contract between you and the company holding your money—like the TSP, your insurance provider, or a brokerage firm. On it, you name the specific person (or people) who will receive the assets from that account after you're gone.

What many people don't realize is that this form is so powerful it legally overrides your will. If your will says one thing and your beneficiary form says another, the beneficiary form wins every time for that specific account.

The Power of Bypassing Probate

One of the biggest benefits of a properly completed beneficiary form is that it allows your assets to skip the probate process. Probate is the court-supervised procedure for settling an estate, and frankly, it can be a nightmare—it's often slow, expensive, and public.

By naming a beneficiary, you create a direct path for your assets to transfer to your loved ones. This "express lane" means they can access funds much faster—often within weeks—rather than waiting months or even years for a court to settle your estate.

For a deeper dive into how these documents are evolving, you can learn more about electronic beneficiary designation forms on esignglobal.com.

Key Functions of the Form

At its heart, this form brings clarity and control to your financial plan. It leaves no room for guessing games or family disputes, which is why it’s a cornerstone of smart estate planning.

Here's a quick look at the core functions of this important document, summarized for clarity.

Key Features of a Beneficiary Designation Form at a Glance

| Feature | What It Means for You | Primary Benefit |

|---|---|---|

| Direct Asset Transfer | You name who gets the account assets directly. | Avoids the lengthy and costly probate court process. |

| Legal Authority | The form's instructions supersede your will for that specific account. | Ensures your wishes for that account are followed without question. |

| Clear Instructions | You can allocate specific percentages to multiple beneficiaries. | Eliminates ambiguity and prevents potential family disputes. |

| Flexibility | You can easily update beneficiaries after major life events. | Keeps your financial plan current with your life circumstances. |

This table shows just how vital this simple piece of paper is in making sure your financial wishes are carried out smoothly and efficiently.

To break it down even further, here's what the form lets you do:

- Specify Primary Beneficiaries: You can name one or more people who are first in line to receive the funds.

- Designate Contingent Beneficiaries: This is your backup plan. You can name secondary beneficiaries who will inherit the assets if your primary choices have already passed away.

- Allocate Percentages: You decide exactly how the money is split. You might give a 50/50 share to two children or divide it differently among family members.

- Update Your Wishes: Life changes. Marriage, divorce, a new baby—these are all moments when you should review your forms. This document makes it simple to keep your designations aligned with your current life.

Why This Form Is a Must-Do for Federal Employees

If you’re a federal employee, getting a handle on beneficiary designation forms isn't just a smart move—it’s an absolutely critical part of protecting your family's financial future. This single document is the final word on who gets your most valuable work-related assets.

Think of it as a direct instruction manual for your benefits. These forms control everything from your Thrift Savings Plan (TSP) nest egg to your Federal Employees' Group Life Insurance (FEGLI) payout. They also determine what happens to your retirement benefits under the Federal Employees Retirement System (FERS) or Civil Service Retirement System (CSRS). This isn't just another piece of government paperwork; it’s a powerful command.

The Government's Default Plan: The Order of Precedence

So, what happens if you never fill one out, or the one on file is invalid? The government won't try to guess what you wanted. Instead, it falls back on a strict, legally mandated sequence called the statutory order of precedence.

This rigid hierarchy dictates who gets your benefits, and it often doesn't match what people actually want. Here’s how it works:

- First, to your surviving spouse.

- If you have no spouse, to your child or children in equal shares.

- If none of the above, to your parents in equal shares.

- If your parents are not living, to the executor or administrator of your estate.

- Finally, to your next of kin according to the laws of your state.

Relying on this default plan is a huge gamble. Your life savings could end up with a distant cousin you haven't seen in years. Worse, if you've gone through a divorce and haven't updated your forms, an ex-spouse could legally receive your benefits. The order of precedence leaves zero room for your personal wishes.

Why Your Will Is Not Enough

This is a big one. A lot of people assume their will or living trust covers all their bases. For federal employees, this is a dangerous and costly misunderstanding. When it comes to assets like your TSP, FEGLI, and FERS/CSRS benefits, the beneficiary designation form is the supreme legal document.

It legally supersedes any instructions in your will. If your will says your TSP goes to your kids, but an old beneficiary form still lists your ex-spouse, that ex-spouse gets the money. End of story. The form’s directive is absolute.

This legal principle is what makes these forms such powerful tools. They bypass probate and override other estate documents for the specific assets they cover. This is a key concept to grasp in estate planning, as explained in a helpful article on how beneficiary designations fit into estate plans on phillipslytle.com.

Real-World Consequences of Neglect

Failing to fill out or update these forms can unleash financial and emotional chaos on your family during an already devastating time.

Imagine a federal employee who gets divorced and remarries but forgets to update their TSP-3 form. Even with a brand-new will naming their current spouse as the sole heir, their entire TSP account—which could be hundreds of thousands of dollars—would legally go to their ex-spouse. It happens more than you think.

Or, consider an unmarried employee with no children. If they have no form on file, their benefits will go to their parents. While that might be fine, maybe they actually wanted to support a sibling with special needs, a lifelong partner, or a charity they cared deeply about. Without the form, those intentions mean nothing.

These aren't just hypotheticals; they are real-life scenarios that underscore why you need to be proactive. You can learn more about protecting your loved ones in our complete guide to federal employee survivor benefits. Taking a few minutes now to check your forms ensures your legacy is handled exactly the way you want, giving you—and your family—true peace of mind.

Navigating Key Federal Beneficiary Forms

Alright, so you understand why beneficiary designations are so important. Now for the practical part: finding and filling out the right paperwork for your federal benefits. This is where the rubber meets the road.

Think of your federal benefits package like a portfolio of different accounts—a TSP account, a life insurance policy, and a pension. Each one is a distinct asset, and each needs its own specific beneficiary form. You can't just fill out one master form and call it a day. Getting this right means ensuring your assets go exactly where you intend them to, without any ambiguity.

Let's walk through the most common forms you'll encounter as a federal employee. I'll break down what each one does and where you can get your hands on it.

Thrift Savings Plan Form TSP-3

Your Thrift Savings Plan (TSP) is often one of the biggest assets you'll build during your career. The only document that tells the TSP who gets that money when you're gone is Form TSP-3, Beneficiary Designation.

Don't skip this, even if you're married. While your spouse has certain legal rights to your TSP, the TSP-3 makes your wishes official. It’s also where you'll name contingent beneficiaries—the essential backup plan in case your primary beneficiary can't inherit the funds.

Thankfully, you can usually handle this online right through your TSP account, which is by far the easiest and most secure way to do it.

Federal Employees' Group Life Insurance Form SF 2823

The life insurance you have through the Federal Employees' Group Life Insurance (FEGLI) program is governed by a different form: SF 2823, Designation of Beneficiary. This is your direct line of communication to the Office of Federal Employees' Group Life Insurance (OFEGLI), telling them who receives your life insurance payout.

A will won't cut it here. I've seen too many people make the mistake of thinking their will can override this form—it can't. The SF 2823 is the only legal document that matters for your FEGLI benefits. To get a deeper dive on this, check out our complete guide to Federal Life Insurance (FEGLI).

This form is absolutely critical. Life insurance is often the first wave of financial support your family receives. An old SF 2823 could accidentally send that money to an ex-spouse, leaving your current family in a tough spot right when they need that help the most.

Federal Retirement System Forms SF 3102 and SF 2808

Your pension doesn't just disappear if you pass away before receiving all your contributions back. There’s a beneficiary component for any lump-sum payment that might be due, and the form you need depends on your retirement system.

- FERS Employees: If you're in the Federal Employees Retirement System, you'll use Form SF 3102, Designation of Beneficiary. This tells OPM who should get any remaining FERS contributions.

- CSRS Employees: For those in the older Civil Service Retirement System, the form you need is SF 2808, Designation of Beneficiary. It serves the exact same purpose, just for the CSRS system.

Without these forms on file, your contributions will be paid out according to the standard order of precedence, which might not reflect what you actually want.

Your Action Plan for These Forms

Knowing about these forms is one thing; actually managing them is another. Your agency's HR office is your go-to resource for getting and submitting paper forms, though more and more can be handled digitally.

To make it simple, here’s a quick-reference guide to the essential forms we just covered.

Essential Beneficiary Forms for Federal Employees

This table is your cheat sheet for the most common beneficiary forms a federal employee will ever need. It covers what they are, what they do, and where to find them.

| Form Number | Benefit Program | Purpose of the Form | Where to Find It |

|---|---|---|---|

| TSP-3 | Thrift Savings Plan | Designates who receives your TSP account balance. | Your online TSP account portal or the TSP website. |

| SF 2823 | Federal Employees' Group Life Insurance (FEGLI) | Specifies who receives your life insurance proceeds. | Your agency's HR office or the OPM website. |

| SF 3102 | Federal Employees Retirement System (FERS) | Names who receives a lump-sum of your FERS contributions. | Your agency's HR office or the OPM website. |

| SF 2808 | Civil Service Retirement System (CSRS) | Names who receives a lump-sum of your CSRS contributions. | Your agency's HR office or the OPM website. |

Taking a few hours to track down, review, and update these documents is one of the most powerful things you can do to protect your family's future. Each form is a direct order, making sure the benefits you worked so hard for end up in the right hands.

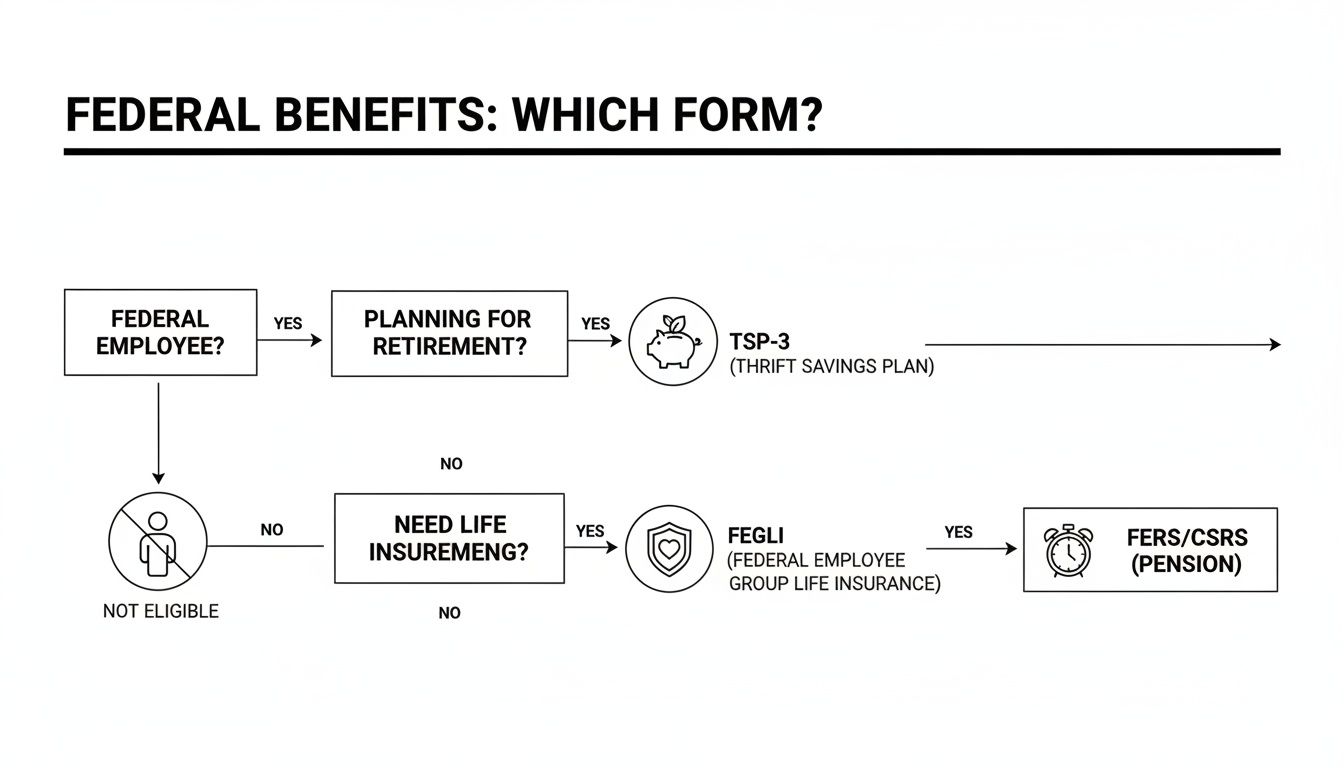

A Practical Guide to Completing Your Designations

Okay, so you know which forms to use. That's a huge step. But the real work is in filling them out correctly to make sure your wishes are followed to the letter. Let's walk through how to do this, turning your intentions into legally binding instructions.

Completing a beneficiary form isn't just about jotting down a name. You need to understand the key difference between your primary and contingent beneficiaries. This simple structure is what creates a clear line of succession for your federal benefits.

This flowchart is a great starting point. It quickly shows you which form goes with which benefit, taking the guesswork out of the process.

As you can see, the visual separates your TSP, FEGLI, and FERS/CSRS benefits and points you directly to the form needed for each one.

Primary vs. Contingent Beneficiaries

This is the most critical concept to get right. Think of it as building a "Plan B" directly into your paperwork. It's a simple idea with powerful implications.

Primary Beneficiary: This is your first choice, the person or entity you want to receive your benefits, no questions asked. You can name more than one primary beneficiary—just make sure you specify the exact percentage each should get (e.g., "My two children, 50% each").

Contingent Beneficiary: This is your backup plan. Your contingent (or secondary) beneficiary only steps in if all of your primary beneficiaries have passed away before you do.

If you don't name a contingent beneficiary and something happens to your primary, your benefits will be paid out according to the standard order of precedence. Naming a backup keeps you firmly in control of where your money goes.

How to Properly Name Your Beneficiaries

When it comes to these forms, clarity is king. You must use full, legal names. No nicknames, no shortcuts like "my kids." Ambiguity here can cause serious legal headaches for your family down the road.

Example: Instead of "My wife, Jane," you need to write her full legal name, such as "Jane Marie Smith." If you’re splitting the benefit among several people, double-check that the percentages add up to exactly 100%.

And remember, you're not just limited to naming people. You can also designate:

- A Trust: This is a very common and effective strategy, especially if you have minor children or beneficiaries with special needs who require long-term financial management.

- A Charity: Want to leave a lasting legacy? You can name a qualified charitable organization to receive all or a portion of your benefits.

- Your Estate: While this is an option, it’s usually not the best one. Naming your estate forces the asset through probate court, which is the very process beneficiary forms are designed to avoid.

The Importance of Regular Reviews

This is not a "set it and forget it" task. Life changes, and your beneficiary forms need to change with it. A designation you made a decade ago might be completely wrong for your life today.

Keeping these forms current is becoming more important than ever. Projections from the Social Security Administration show a growing need for services related to managing these types of designations, a trend that's expected to continue. You can read more about these demographic trends on ssa.gov. This data just reinforces what we already know: people are recognizing how vital it is to stay on top of these documents.

As a rule of thumb, review your forms every 3-5 years. More importantly, certain life events should be an automatic trigger to pull them out and make sure they’re still accurate.

Trigger Events for Updating Your Forms

Think of this list as your personal alert system. If any of these things happen in your life, put "review beneficiary forms" at the top of your to-do list.

- Marriage or Divorce: This is by far the most common reason for an update—and the one that causes the most problems when ignored.

- Birth or Adoption of a Child: As your family grows, your financial plans need to grow with it.

- Death of a Named Beneficiary: If a primary beneficiary passes away, your contingent beneficiary moves into the primary spot. You'll likely want to name a new contingent beneficiary.

- A Minor Child Reaching Adulthood: The trust you set up for a minor might no longer be needed once they are a legal adult, simplifying your plan.

- Significant Change in Financial Situation: A major change in your financial status—or a beneficiary's—might change how you want to distribute your assets.

Staying on top of these forms is the single best way to ensure your hard-earned benefits end up exactly where you want them, providing for your loved ones as you intended.

Common Mistakes and How to Avoid Them

Learning from where others have gone wrong is one of the smartest ways to protect your legacy. A beneficiary designation form is a powerful document, but a few simple mistakes can completely derail your wishes, causing immense heartache and financial strain for the people you care about most.

These aren't obscure, technical errors. They're common oversights that happen every single day. By understanding these pitfalls now, you can make sure your federal benefits are distributed exactly as you intend.

Failing to Update After Life Events

This is, without a doubt, the single biggest and most damaging mistake we see. A beneficiary form is not a "set it and forget it" document. Think of it as a snapshot of your life at a specific moment—and when your life changes, your forms must change, too.

A major life event like a divorce is a huge red flag. An old form naming an ex-spouse could legally send your entire TSP or FEGLI payout to them, no matter what your will says. Marriage, the birth of a child, or the death of a named beneficiary are all moments that should trigger an immediate review.

On average, accounts with a clear, current beneficiary are processed much faster, sometimes cutting down delays by several months. This simple update ensures your loved ones get the financial support they need without a long and stressful wait.

Naming a Minor Child Directly

Naming your child as your beneficiary feels like the most natural thing in the world. But listing a minor directly on the form can create a legal nightmare. By law, financial institutions can't just hand over large sums of money to a child.

If a minor is named, the funds are essentially frozen. A court has to get involved to appoint a legal guardian to manage the money until the child comes of age (typically 18 or 21). This court process is public, it's expensive, and it's slow. Worst of all, the person the court appoints to manage the funds might not be who you would have chosen.

A much better strategy is to work with an estate planning attorney to set up a trust for your child's benefit. This could be a Uniform Transfers to Minors Act (UTMA) account or a living trust. You then name the trust as the beneficiary on your form, which provides clear, legally-binding instructions for how the money should be managed for your child's care and future.

Forgetting the Contingent Beneficiary

So many people carefully name their primary beneficiary—often their spouse—and then just stop there. This creates a massive hole in your plan. What happens if your primary beneficiary passes away at the same time as you, or even just a few days before?

Without a backup, or contingent beneficiary, the asset is treated as if you never filled out a form at all. It will then be paid out according to the government’s rigid order of precedence. This could send your assets to a distant relative you barely know instead of, for example, your siblings or a favorite charity.

- Your Action Plan: Always, always name a contingent beneficiary. Think of it as essential insurance for your estate plan. It’s your backup instruction that keeps you in control, no matter what happens.

Being Vague or Using Incorrect Names

Ambiguity is the absolute enemy of a beneficiary designation. Using unclear terms or incorrect information is an open invitation for disputes and delays.

Some of the most common errors include:

- Using nicknames: Listing "Aunt Sue" instead of her full legal name, "Susan M. Johnson."

- General descriptions: Writing "my children" instead of naming each child individually with their full legal name.

- Misspelled names or old addresses: Even tiny clerical errors can create huge hurdles for your heirs when they try to claim their benefits.

Be painfully specific. Use full legal names and clearly state the percentage of the benefit each person should receive. Before you sign, double-check that all the shares add up to exactly 100%. Taking a few extra minutes to get these details right can save your family months of frustration and ensure your legacy is handled smoothly, honoring your wishes without any complications.

Your Next Steps to Secure Your Financial Legacy

We've covered a lot of ground, but it all boils down to this: a simple beneficiary designation form is one of the most powerful legal documents you have. It's your direct line of control, ensuring your hard-earned benefits—from your TSP to your life insurance—end up exactly where you want them, without the headaches and costs of probate.

If there's one thing to take away from all this, it's that this form legally overrides your will for the specific account it's tied to. That's a huge deal. It's why keeping your designations up-to-date isn't just a suggestion; it's one of the most critical parts of your financial life. An old form can accidentally send your entire life savings in the wrong direction, causing a world of hurt for the people you love.

Your Immediate Action Plan

Feeling ready to get this handled? Good. Don't put it off. Here’s a straightforward checklist to get you started right now and make sure your wishes are locked in.

- Hunt Down Your Forms: Go find the most recent beneficiary forms for all your federal accounts. We're talking about the TSP-3, SF 2823 (FEGLI), and either the SF 3102 (FERS) or SF 2808 (CSRS).

- Review Every Single Detail: Look closely at the names. Are your primary and contingent beneficiaries still correct? Are their full legal names spelled perfectly? Do the percentage splits still make sense for your life today?

- Update What's Broken: If you see anything that's wrong—an ex-spouse still listed, a new child missing—fix it now. Don't wait. Log into your online accounts or get in touch with HR to submit the updated forms immediately.

Real peace of mind isn't just about having a plan; it's about knowing that plan is in perfect order. Checking these documents isn't just a financial chore. It's an act of love—protecting your family from stress and confusion when they'll need it least.

Getting a professional eye on these forms can ensure they work seamlessly with the rest of your estate plan. To get a better handle on the big picture, you can find a ton of great information by navigating federal employee death benefits in our comprehensive guide.

Here at Federal Benefits Sherpa, our entire focus is helping federal employees like you get this right. We can help you get rid of the guesswork, confirm every designation is perfect, and make sure your legacy is protected, exactly the way you want.

Answering Your Top Questions About Beneficiary Designations

Let's clear up some of the most common questions federal employees have about these critical forms. Getting these details right is a huge part of protecting your family and your legacy.

What Happens if I Don't Have a Beneficiary Form on File?

This is a big one. If you pass away without a valid beneficiary form on file, the government doesn't try to figure out what you might have wanted. Instead, it follows a strict, legally-mandated formula called the statutory order of precedence.

This default plan is inflexible. Your assets will typically go to your surviving spouse first. If you don't have a spouse, it goes to your children in equal shares, then to your parents, and so on. While that might work for some, it can easily sideline a long-term partner, a favorite niece, or a charity you cared about.

Can I Name a Trust as My Beneficiary?

Yes, and this is often a smart move. Naming a trust as your beneficiary is a powerful estate planning tool, especially if you have minor children who can't legally inherit large sums of money directly. It's also incredibly useful for providing long-term financial care for a beneficiary with special needs.

By designating a trust, you ensure your assets are managed exactly according to the rules you've set up. This gets into complex legal territory, though, so I always recommend working with an estate planning attorney to make sure the trust is set up and named correctly on all your forms.

How Often Should I Review My Beneficiary Forms?

Think of it like a regular check-up for your financial plan. A good rule of thumb is to pull out your forms and review them every 3-5 years. Life changes, and your plans need to change, too.

More importantly, certain life events should be an immediate trigger to review your designations. These are moments when your personal circumstances shift dramatically, and your paperwork needs to catch up.

You should always check your forms after:

- Getting married or divorced.

- The birth or adoption of a child.

- The death of someone you named as a beneficiary.

- Any other significant change in your family or financial situation.

Keeping these documents current is one of the simplest yet most important things you can do to make sure your hard-earned benefits end up in the right hands, without any complications.

Navigating the maze of federal benefits can feel like a full-time job, but you don't have to go it alone. The experts at Federal Benefits Sherpa are here to help federal employees make sense of these crucial decisions and secure a stress-free retirement. Schedule your free 15-minute benefits review today to get peace of mind that your financial legacy is protected. You can learn more at https://www.federalbenefitssherpa.com.