A Federal Employee’s Guide to TSP Rules for Withdrawal

The TSP rules for withdrawal hinge on a few key factors: your employment status, your age, and what you need the money for. At a high level, the rules break down into in-service withdrawals (for when you're still working), post-separation withdrawals (after you've left your federal job), and eventually, required minimum distributions (RMDs).

Figuring out which set of rules applies to you is the first, and most important, step in accessing your money without a hitch.

Decoding Your TSP Withdrawal Options

I like to think of the Thrift Savings Plan as a financial reservoir you've spent your entire career filling. The various TSP rules for withdrawal are simply the different faucets attached to it. Each one serves a unique purpose and controls how your money flows out.

Some faucets are for emergencies while you're still working. Others are designed to provide a steady, predictable income stream once you retire. And some let you take out a large amount all at once. Knowing which faucet to turn—and when—is the key to managing your financial future.

This guide is designed to walk you through every option, so you can feel confident in your decisions and align them with your long-term goals. We’ll break down the complex regulations into simple, actionable advice.

To get started, let's look at a quick summary of your main options.

At-a-Glance TSP Withdrawal Types and Timings

This table provides a high-level overview of the primary ways you can access your TSP funds, helping you quickly identify which category your needs might fall into.

| Withdrawal Type | Eligibility (When You Can Take It) | Primary Purpose |

|---|---|---|

| In-Service Withdrawal | While still a federal employee; must be age 59½ or have a financial hardship | To access funds for a specific, urgent need or goal while you are still working. |

| Post-Separation Withdrawal | After you have officially separated or retired from federal service. | To start using your TSP savings for retirement living expenses or other goals. |

| Installment Payments | A type of post-separation withdrawal. | To create a regular, predictable income stream in retirement. |

| Annuity | A type of post-separation withdrawal. | To convert your TSP balance into a guaranteed lifetime income payment. |

Each of these serves a different purpose, and the best choice really depends on your personal financial picture.

The Four Main Categories of TSP Withdrawals

Your ability to tap into your TSP account is governed first and foremost by whether you're still working for the government or have already separated. Each path comes with its own set of rules and strategic trade-offs.

Here are the four primary ways you can take money out:

- In-Service Withdrawals: These are available to active employees who've hit certain milestones, like reaching age 59½ or experiencing a documented financial hardship.

- Post-Separation Withdrawals: This is the most common path. Once you leave federal service, you have maximum flexibility to take partial or full distributions as needed.

- Installment Payments: A popular choice after separation, this option lets you set up a regular, predictable income stream, almost like a personal pension.

- Annuities: You can also choose to use some or all of your TSP balance to purchase an annuity, which provides a guaranteed income stream for life through a private insurance company.

It's worth remembering how much things have changed. The TSP Modernization Act of 2017 completely overhauled the old, restrictive rules. For example, you’re no longer stuck with a one-time partial withdrawal after you separate—you can now take them whenever you need to.

This added flexibility is huge. It allows you to treat your TSP more like a modern, dynamic retirement account that can adapt as your life changes. The official TSP website has all the tools and forms you'll need to get started.

You can dive deeper into structuring these payouts in our complete guide to Thrift Savings Plan withdrawal options. Just remember that every choice you make has distinct tax consequences and will impact your long-term financial security, which is exactly what we'll explore next.

Understanding Your TSP Withdrawal Options After You Leave Federal Service

Once you hang up your hat and separate from federal service, your Thrift Savings Plan account gets a major promotion. It's no longer just a place to save money; it becomes a powerful toolkit for generating your retirement income. The rules for taking money out after you've separated are designed to be flexible, giving you the control to build an income stream that fits your life.

Think of your TSP balance as a pile of lumber. The various withdrawal options are your saws, hammers, and measuring tapes—the tools you'll use to construct a sturdy financial house for your retirement years.

This level of flexibility is actually a pretty recent development. Not long ago, the TSP rules for withdrawal were incredibly restrictive. Retirees were often forced to make a single, irreversible decision right at the start. Thankfully, things have changed for the better, and now you have a dynamic set of options you can adjust as life unfolds.

A New Era of Flexibility

The TSP Modernization Act completely changed the game for federal retirees. The new rules, which kicked in on September 15, 2019, introduced much more flexible withdrawal options and got rid of an old, frustrating rule that could sometimes lead to account forfeiture. If you're interested in the nitty-gritty details, you can find a comprehensive overview in the Department of Labor's audit report on the withdrawal process.

What this all means for you is that you’re no longer locked into a single choice. You can now mix and match different withdrawal methods throughout your retirement, giving you an incredible amount of control over your own money.

So, let's open up that post-separation toolkit and see what you've got.

Tool 1: Partial Withdrawals

Think of a partial withdrawal as your go-to problem solver. It lets you pull out a specific chunk of cash whenever you need it, as long as the amount is $1,000 or more. You can request these as often as you want, with only a 30-day waiting period between each one.

This option is perfect for those larger, one-time expenses that pop up in retirement without messing up your regular monthly budget.

- Big-Ticket Home Repairs: When the roof finally gives out or the AC unit dies in July, a partial withdrawal can cover the cost.

- Buying a New Car: You can grab a portion of your TSP funds to pay for a reliable vehicle instead of getting stuck with a high-interest car loan.

- Unexpected Medical Bills: For healthcare costs that insurance doesn't fully cover, this gives you quick access to the funds you need.

Before the Modernization Act, you were allowed only one partial withdrawal for your entire retirement. Now, you can take them as needed, which makes your TSP a much more practical and useful financial resource.

The Bottom Line: Partial withdrawals are your best bet for lump-sum needs. They give you the precision to handle specific financial goals or emergencies without derailing your long-term plan.

Tool 2: Installment Payments

If partial withdrawals are for special projects, installment payments are the workhorse designed to build your steady, reliable retirement paycheck. This option lets you set up recurring, automatic payments from your TSP, creating a predictable cash flow to cover your day-to-day living expenses.

And the best part is, you're in the driver's seat. You decide on the frequency and the amount.

- How Often: You can choose to get your payments monthly, quarterly, or even just once a year.

- How Much: You can set a fixed dollar amount (like $1,500 per month) or ask the TSP to calculate a payment based on your life expectancy.

What makes this tool so valuable is that nothing is set in stone. You can start, stop, or change the amount of your installment payments whenever you want. If inflation hits and your costs go up, you can increase your payments. If you come into some other money and don't need as much from your TSP, you can reduce them or even pause them completely. This adaptability is why it’s one of the most popular TSP rules for withdrawal among federal retirees.

Tool 3: The Full Withdrawal (Lump-Sum Payment)

The final tool in your kit is the full withdrawal, often called a single or lump-sum payment. Just as the name implies, this allows you to take out your entire TSP account balance in one go. While having all your cash in hand might sound appealing, this option comes with some serious strings attached.

Taking a full withdrawal is almost guaranteed to land you a massive tax bill for the year you take the money, and it could easily push you into a much higher tax bracket. Because of this, it’s typically used for very specific strategic moves, not as a general retirement income strategy.

When a Full Withdrawal Might Make Sense:

- Rolling Over to an IRA: By far the most common reason is to move your entire TSP balance into an Individual Retirement Account (IRA). An IRA can offer a much wider universe of investment choices, from individual stocks to specialized funds.

- A Major Life Purchase: In some rare cases, a retiree might use a full withdrawal for an enormous purchase, like buying a dream retirement home with cash.

Keep in mind that choosing this path closes your TSP account for good. It's a final decision that demands a lot of careful thought and planning. For the vast majority of federal retirees, a smart combination of partial withdrawals and installment payments creates a far more tax-efficient and sustainable income plan for the long haul.

Accessing Your TSP While Still Working: In-Service Withdrawals

What happens when you need money from your retirement savings before you've left your federal job? While the Thrift Savings Plan is built for the long haul, life happens. Fortunately, certain TSP rules for withdrawal allow you to access your funds while you’re still an active employee. These are called in-service withdrawals, and they come in two very different flavors.

One is a lifeline for true financial emergencies, while the other is an age-based option offering more flexibility as you get closer to retirement. Understanding the strict rules for each is absolutely critical to avoid nasty penalties and make a smart financial move.

Financial Hardship Withdrawals

A financial hardship withdrawal is exactly what it sounds like—a way to get cash for a serious and immediate financial need. The TSP has very specific criteria for what qualifies, and you'll need the documents to prove it. This isn't a loan you pay back; it's a permanent withdrawal that shrinks your retirement nest egg.

You can only request a hardship withdrawal for one of these four reasons:

- Recurring Negative Cash Flow: When your monthly expenses are consistently higher than your income.

- Medical Expenses: For medical bills (including for household members) that your insurance won’t cover.

- Personal Casualty Losses: To cover uninsured losses from events like fires, floods, or major storms.

- Legal Fees: For attorney fees and court costs related to a separation or divorce.

It's vital to know that this option comes with serious strings attached, including taxes and potential penalties. Think of it as a last resort after you've explored every other possible avenue. We cover this in much more detail in our guide on TSP hardship withdrawal rules.

Age-Based In-Service Withdrawals

Once you hit age 59½, a new door opens. The TSP lets you take an age-based in-service withdrawal without having to prove any kind of financial hardship. This gives you a ton of flexibility for whatever you need, whether it's a home renovation project or wiping out some high-interest debt.

You can take up to four age-based withdrawals per calendar year, but you must wait at least 30 days between each request. This rule is in place to encourage thoughtful planning rather than frequent, small dips into your account.

This is a powerful tool. It lets you tap into your retirement funds without separating from service, providing a financial boost when you might need it most. But just because you can take the money doesn't always mean you should. Every dollar you pull out is a dollar that's no longer invested and growing for your future.

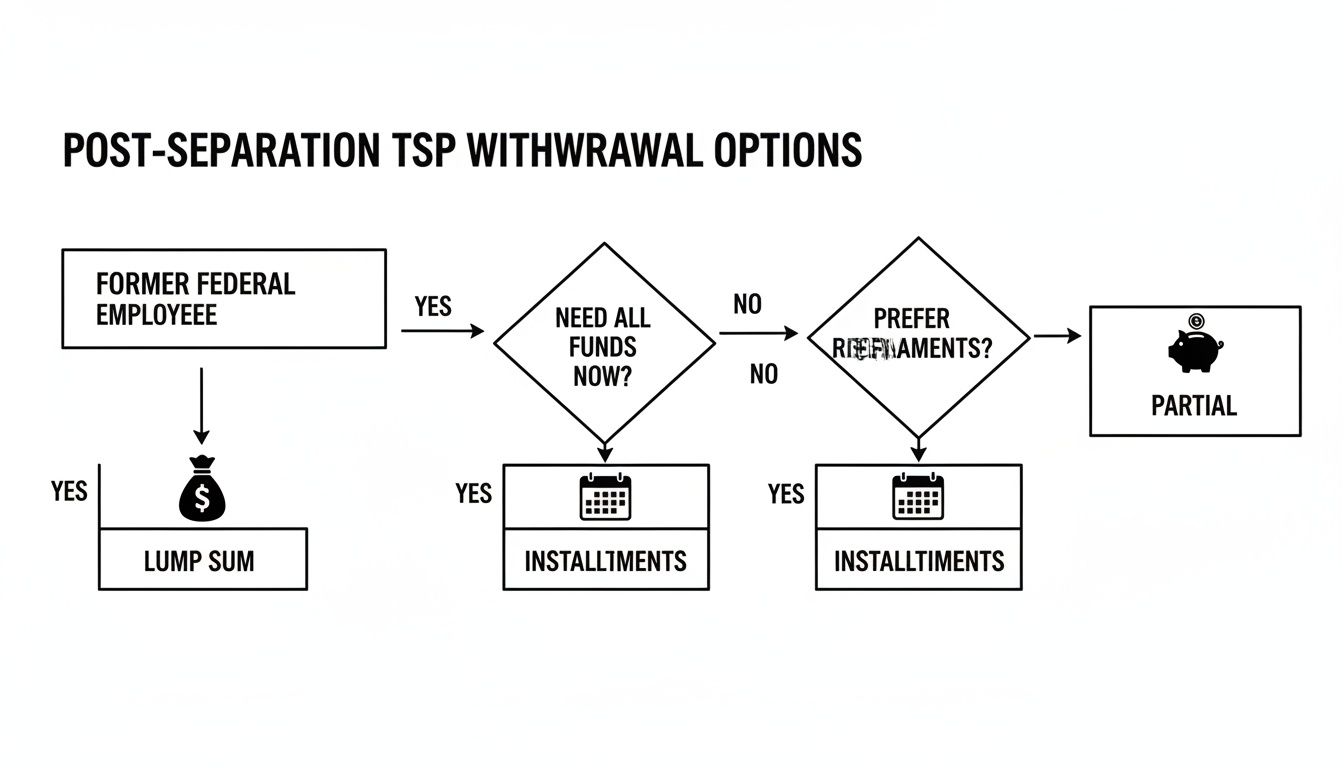

The flowchart below shows the different paths you can take once you've actually left federal service.

While this visual focuses on post-separation options, it helps illustrate how different withdrawal types—like partials or installments—are designed to meet unique financial needs after your federal career is over.

Important Considerations and Trends

No matter which type of in-service withdrawal you take, the IRS sees it as taxable income for that year. If you're under 59½ and take a hardship withdrawal, you’ll also likely get hit with a 10% early withdrawal penalty on top of the income taxes you owe.

Recent data shows a clear trend. According to the 2024 Thrift Savings Plan data, hardship withdrawals are on the rise, with 3.9% of participants taking one. While the 40-49 age group has historically been the highest user, the 30-39 age group has recently claimed the second spot with a usage rate of 5.46%. You can dig into the numbers yourself in the TSP Annual Report for 2024.

Ultimately, taking an in-service withdrawal is a major financial decision. You have to weigh the immediate benefit against the long-term cost to your retirement savings before you move forward.

The Tax Consequences of TSP Withdrawals

Getting a handle on the different TSP rules for withdrawal is just the first step. The real test is understanding how taxes are going to impact the money you finally take out. If you don't plan for the tax man, you could be in for a nasty surprise with a smaller check than you budgeted for and an unexpected bill from the IRS.

How your withdrawal gets taxed boils down to one simple question: is the money coming from your Traditional TSP or your Roth TSP? The answer changes everything, since they were funded with different types of dollars from the very beginning.

Traditional TSP Withdrawals

Remember all those years you contributed to your Traditional TSP? You did that with pre-tax dollars, which gave you a nice little tax break each year by lowering your taxable income. Well, now it's time to pay the piper. The trade-off for that upfront benefit is that you have to pay income taxes on that money—and all the growth it generated—when you pull it out in retirement.

Think of it this way: your Traditional TSP is a tax-deferred pot. Every single dollar you withdraw, whether it was part of your original contribution or from decades of earnings, is taxed as ordinary income. It’s simply added to your other income for the year and taxed at whatever your current federal and state rates are.

Roth TSP Withdrawals

The Roth TSP is the complete opposite. You funded it with after-tax dollars, so there was no tax deduction when you put the money in. But here's where the magic happens: as long as you play by the rules, every withdrawal you make in retirement is 100% tax-free.

To unlock that incredible tax-free benefit, your withdrawal has to be "qualified." This is a key term, and it means two simple conditions have been met:

- You are at least age 59½.

- It's been at least five years since January 1st of the calendar year you made your very first Roth TSP contribution.

Check both of those boxes, and every penny you take out—your contributions and all the earnings—is yours to keep, with no bill from Uncle Sam. For those looking for even more ways to manage their tax-free money, transferring TSP funds to a Roth IRA can open up additional planning strategies.

Let's break down the core differences in how these withdrawals are taxed.

Traditional vs. Roth TSP Withdrawal Tax Rules

| Feature | Traditional TSP | Roth TSP |

|---|---|---|

| Contributions | Made with pre-tax dollars. | Made with after-tax dollars. |

| Tax on Withdrawals | Both contributions and earnings are taxed as ordinary income. | Both contributions and earnings are tax-free if the withdrawal is "qualified." |

| Qualification Rules | No specific qualification rules, but penalties may apply for early withdrawal. | Must be age 59½ and meet the 5-year rule for earnings to be tax-free. |

| Tax Impact | Increases your taxable income in retirement. | Does not increase your taxable income in retirement. |

This table really highlights the fundamental trade-off: pay taxes now (Roth) or pay taxes later (Traditional).

The Pro-Rata Rule for Mixed Accounts

So, what happens if you’re like most federal employees and have money in both Traditional and Roth TSP accounts? This is where a critical, and often misunderstood, concept called the pro-rata rule comes into play. The TSP views your entire account as a single entity when you request a withdrawal.

Imagine your TSP is a big glass jar filled with two kinds of marbles: black marbles representing your taxable Traditional money and clear marbles for your tax-free Roth money. If your account is 80% black marbles and 20% clear ones, you can’t just reach in and pull out only the clear, tax-free ones. Any scoop you take will reflect that same ratio: 80% black and 20% clear.

In real-world terms, this means every withdrawal you take from a mixed account will be proportionally split between your Traditional and Roth balances. You can't just drain the Roth side first. This is a foundational part of the TSP rules for withdrawal that catches many people off guard.

The 10 Percent Early Withdrawal Penalty

On top of ordinary income taxes, there's another potential pitfall to be aware of: the 10% early withdrawal penalty. If you take money out of your TSP before you hit age 59½, the IRS generally tacks on this extra penalty to any taxable portion of your withdrawal.

Fortunately, there are several key exceptions that can help you avoid this sting:

- The Rule of 55: If you separate from federal service during or after the calendar year you turn 55, you can take withdrawals from your TSP without penalty.

- Special Category Employees: Federal law enforcement, firefighters, and air traffic controllers have a special provision allowing for penalty-free withdrawals if they separate in the year they turn 50 or later.

- Permanent Disability: If you become totally and permanently disabled, the penalty is waived.

- Substantially Equal Periodic Payments (SEPP): You can arrange for a series of calculated payments based on your life expectancy, governed by IRS Rule 72(t).

Knowing these exceptions is absolutely vital if an early retirement is in your plans. It could be the difference between keeping your money and handing an extra 10% of it over to the IRS. As always, be sure to check the latest TSP and IRS publications, as the rules can and do change.

Strategic Withdrawal Planning for a Secure Retirement

Knowing the individual TSP rules for withdrawal is one thing. But weaving them into a cohesive retirement income strategy is what truly builds a secure financial future. It’s a bit like learning the rules of chess; you have to know how each piece moves, but winning the game requires a plan that coordinates all your pieces on the board.

Your TSP is a major piece on that board, but it doesn't operate in a vacuum. It has to work in harmony with your other income sources, like your FERS or CSRS pension and your Social Security benefits. A smart strategy isn't just about pulling money out—it's about sequencing those withdrawals to make your money last and keep your tax bill as low as possible.

Building Your Income Foundation with the 4% Rule

For many retirees, a great starting point is the "4% Rule." This isn't some official TSP regulation, but rather a widely accepted guideline for creating a sustainable income stream in retirement. It gives you a simple but powerful framework for figuring out how much you can safely withdraw each year without a high risk of running out of money.

The 4% withdrawal rule provides federal employees with a practical way to manage their Thrift Savings Plan distributions. The guideline suggests that a retiree can safely withdraw 4% of their account balance in the first year of retirement, and then adjust that amount for inflation in subsequent years. For example, if you have a $400,000 TSP balance, this rule would suggest an initial withdrawal of $16,000 for the year, or about $1,333 per month. You can find more details on this retirement strategy in a report from the National Association of Letter Carriers.

This rule helps you establish a baseline income from your TSP, turning that big lump sum into a predictable cash flow you can plan around.

Sequencing Your Withdrawals for Maximum Impact

Once you have a baseline, the next step is to coordinate all your income streams. Think of yourself as the conductor of an orchestra. You want each instrument—your pension, Social Security, and TSP—to come in at just the right time to create a harmonious financial picture.

Here’s a common strategic approach many federal retirees use:

Pension First: Your FERS or CSRS pension provides a stable, guaranteed income floor. This is your most reliable money, so it should be used to cover your essential, non-negotiable living expenses.

Delay Social Security: If you can afford to, delaying Social Security until age 70 can dramatically increase your monthly benefit. For every year you delay past your full retirement age, your benefit grows by about 8%. That’s a guaranteed return you can’t get anywhere else.

Bridge the Gap with TSP: This is where your TSP becomes a powerful tool. You can use withdrawals from your TSP to act as a "bridge" income during the years between retirement and when you start taking Social Security.

This strategy allows you to use your TSP funds to fill the income gap in your early retirement years. In doing so, you protect your largest potential income source (Social Security), letting it grow to its maximum potential for later in life when you might need it most.

A Practical Scenario

Let's look at a real-world example. Imagine a federal employee, Sarah, who retires at age 62. Her FERS pension is enough to cover her basic living costs, but she wants more income for travel and her hobbies.

Instead of claiming her Social Security right away, she decides to wait until she turns 70.

- Ages 62-69: To supplement her pension, Sarah sets up a combination of monthly installment payments and takes a few partial withdrawals from her TSP. This gives her the extra "fun money" she needs without touching her growing Social Security benefit.

- Age 70 and Beyond: She finally turns on her maximized Social Security benefit. At this point, she can significantly reduce her TSP withdrawals, allowing the remaining balance to keep growing for any future needs or unexpected medical expenses down the road.

By sequencing her income this way, Sarah creates a much more robust and sustainable retirement plan. She leverages each of her assets for its intended purpose, turning a set of abstract rules into a concrete strategy for a comfortable and truly secure retirement.

Your Top TSP Withdrawal Questions, Answered

Even when you think you have a handle on the TSP, the details can get tricky. Federal employees often run into specific situations that leave them wondering what to do next. This section is designed to tackle the most common and crucial questions we hear day in and day out, giving you clear, straightforward answers.

Think of this as the troubleshooting guide for your TSP withdrawal plan. We'll get into the finer points and clear up common areas of confusion so you can manage your retirement funds with confidence.

What Are the Required Minimum Distribution (RMD) Rules for the TSP?

Once you hit a certain age, Uncle Sam says you have to start taking money out of your tax-deferred retirement accounts, whether you need it or not. These are called Required Minimum Distributions, or RMDs, and your TSP is no exception. For most folks, this starts at age 73.

The good news is that the TSP makes this pretty painless. Each year, they'll calculate the minimum amount you’re required to withdraw based on your account balance and the IRS Uniform Lifetime Table.

Here's a great feature of the modern TSP: if you haven't taken out enough money by the RMD deadline, the TSP will automatically send you the difference. This is a fantastic safeguard that keeps you from accidentally getting hit with a huge penalty for forgetting.

This automatic payout protects you from the massive 25% tax penalty the IRS can slap on any RMD amount you fail to withdraw on time. It’s a critical backstop that ensures you stay compliant.

Can I Change My TSP Installment Payments After I Start Them?

This question comes up all the time, and the answer is a big, unequivocal yes. The flexibility of installment payments is one of the best things about the post-separation TSP rules for withdrawal. You are never locked into the payment schedule you originally set up.

Life in retirement isn't static—your income needs can shift from one year to the next. The TSP gets this, and they let you make adjustments whenever you need to.

- Change the Amount: You can raise or lower the dollar amount of your payments to match your budget.

- Change the Frequency: Feel free to switch between monthly and quarterly payments, or the other way around.

- Stop and Restart: If you have other income sources for a while, you can pause your payments entirely and then restart them later.

This level of control allows you to actively manage your cash flow. If the market has a great year, you might decide to take out a bit more. If a big, unexpected expense pops up, you can adjust your payments to cover it. You're in the driver's seat.

How Do TSP Loans Affect My Withdrawal Options?

Leaving federal service with an outstanding TSP loan adds another layer to your withdrawal plan. It’s important to know you can't just keep the loan active after you leave your job. Once you separate, you have two main ways to deal with it.

First, you can pay the loan back in full. If you have the cash on hand, this is often your best bet, as it keeps your entire TSP account balance intact and working for you in retirement.

The second option is to do nothing. If you don't repay the loan, the TSP will declare a "taxable distribution." This means the outstanding loan balance, plus any interest, is treated as if you withdrew it. It gets taxed as ordinary income for that year, and if you're under age 59½, you'll also get hit with the 10% early withdrawal penalty.

A Word of Caution: Before you separate, carefully think through the tax hit of a loan distribution versus the cost of paying it off. A large loan balance can trigger a surprisingly big tax bill in your first year of retirement if you're not prepared.

What Happens to My TSP If I Pass Away?

Planning for your beneficiaries is one of the most important things you can do with your TSP. When you die, the money in your account is paid out based on the most recent valid beneficiary form on file—the Form TSP-3. It's critical to understand that this form overrules anything you've written in a will or a trust.

After you pass away, your designated beneficiaries have a few different options for how to receive the money.

- Spousal Beneficiaries: A surviving spouse gets some unique choices. They can roll the inherited TSP funds into their own TSP account or an IRA. They can also open a beneficiary participant account, which lets the money stay invested in the TSP funds while they take distributions over time.

- Non-Spouse Beneficiaries: Other beneficiaries, like children, can also open a beneficiary participant account to manage the inheritance within the TSP system. Their other options include taking a full or partial lump-sum payment or rolling the money directly into an inherited IRA.

Each of these paths has its own tax rules and distribution deadlines, especially with the 10-year payout rule now in effect for most non-spouse beneficiaries. Keeping your beneficiary designations updated is one of the simplest yet most powerful estate planning moves you can make.

Making sense of your federal benefits is a crucial step toward a secure retirement. At Federal Benefits Sherpa, we specialize in helping federal employees like you map out a clear and confident path forward. To ensure your TSP strategy works in harmony with your overall retirement plan, we invite you to book a free 15-minute benefit review with our team. Let us help you maximize your benefits by visiting us at Federal Benefits Sherpa.