Transferring TSP to Roth IRA A Practical Guide

Thinking about moving your Thrift Savings Plan (TSP) funds into a Roth IRA? It's a big decision, a real crossroads in your financial journey. You're essentially weighing the promise of tax-free income down the road against a pretty hefty, immediate tax bill.

Ultimately, the right answer depends entirely on your personal retirement goals, where you stand financially today, and what you think tax rates will look like in the future.

Is Transferring Your TSP to a Roth IRA the Right Move?

Let's cut to the chase. Moving money from a traditional TSP to a Roth IRA comes down to one simple trade-off: pay taxes now or pay them later. This move takes your pre-tax retirement money, which has been growing tax-deferred, and converts it into post-tax funds. It’s a powerful strategy, but one that comes with a significant upfront cost.

Getting your head around this core concept is the first real step in figuring out if this move aligns with your vision for retirement.

The Big Upside: Why You'd Consider It

The main draw of a Roth IRA is crystal clear: tax-free withdrawals in retirement. Once your money is in that Roth account and you've met the requirements, every qualified dollar you take out—your original contribution and all the earnings—is yours. No federal income tax.

This is a game-changer, especially if you think you’ll be in the same or even a higher tax bracket when you retire.

Beyond the tax benefits, a Roth IRA throws open the doors to a world of investment choices that the TSP, with its limited fund lineup, just can't match. You suddenly gain the freedom to invest in things like:

- Individual stocks and bonds

- An almost endless variety of Exchange-Traded Funds (ETFs)

- Thousands of different mutual funds

- Real Estate Investment Trusts (REITs) and other alternative investments

This kind of control allows you to build a portfolio that truly reflects your personal risk tolerance and financial goals. It’s a level of customization you simply don’t get with the C, S, I, F, and G funds.

The Immediate Downside: The Tax Bite

Here's the catch, and it's a big one: taxes. When you make the transfer, every dollar you move is treated as ordinary income for that year.

So, if you convert $100,000 from your traditional TSP to a Roth IRA, your taxable income for the year instantly jumps by $100,000. That could easily bump you into a higher tax bracket and leave you with a substantial tax bill come April. You have to be prepared to pay those taxes, preferably with money from outside your retirement accounts.

This entire strategy became an option for everyone back in 2010. That's when the Tax Increase Prevention and Reconciliation Act of 2005 officially removed the income limits for Roth conversions, opening the door for any taxpayer to make this move.

It’s also crucial to distinguish between your TSP's traditional and Roth balances. If you’ve been contributing to the Roth TSP, you can roll those funds directly into a Roth IRA without any tax hit—a simple, tax-free transfer. Our guide on what a TSP Roth is and how it maximizes tax-free growth digs into that. This article, however, is focused on the taxable conversion of traditional, pre-tax TSP money.

TSP to Roth IRA Transfer Key Considerations

To help you weigh the pros and cons at a glance, here’s a quick breakdown of what you're facing. This table summarizes the core trade-offs involved in making the move.

| Factor | Potential Advantage (Why You Would) | Potential Disadvantage (Why You Might Not) |

|---|---|---|

| Tax Treatment | All qualified withdrawals are 100% tax-free in retirement. | You must pay ordinary income tax on the entire converted amount upfront. |

| Future Taxes | You're protected if you believe income tax rates will be higher in the future. | If tax rates go down in the future, you might have overpaid in taxes. |

| Investment Options | Access to a virtually unlimited selection of stocks, bonds, ETFs, and mutual funds. | The TSP's streamlined, low-cost index funds are simple and effective for many. |

| Estate Planning | Roth IRAs have no Required Minimum Distributions (RMDs) for the original owner. | The TSP has its own withdrawal requirements you'd be leaving behind. |

| Complexity & Cost | You gain more direct control and can work with a chosen financial advisor. | The TSP is known for its extremely low administrative fees. |

Deciding whether to make this move is a significant financial step. It's less about a "right" or "wrong" answer and more about what aligns with your personal financial forecast and retirement strategy.

The Tax Bill: What Your Conversion Will Really Cost You

Let's get right to the heart of the matter: the immediate tax bill. This isn't some small detail you can figure out later; it's the single biggest cost of moving your traditional TSP funds into a Roth IRA. When you take money from a pre-tax account like the TSP and roll it into a post-tax Roth, the entire amount you convert gets added to your taxable income for the year.

Think of it like getting a surprise bonus at work. It's great, but it comes with a hefty tax consequence. You absolutely have to plan for this hit upfront to avoid a nasty surprise when you file your return.

How This Hits Your Taxable Income

The logic here is pretty straightforward. You're finally paying taxes on money that has never been taxed. Your traditional TSP contributions and all their earnings grew tax-deferred, and now the IRS is ready to collect.

The converted amount isn't taxed as a capital gain. Instead, it’s treated as ordinary income and taxed at your marginal rate. That’s a crucial distinction. It means a big enough conversion can easily bump you into a higher federal income tax bracket.

A lot of people assume there's some special, softer tax calculation for a conversion. There isn't. The IRS sees a $50,000 conversion exactly the same way it sees an extra $50,000 in salary.

A Real-World Conversion Scenario

Let's make this real. Imagine a married couple, both 60, who file their taxes jointly. Their combined taxable income is $190,000, which for 2024 puts them squarely in the 22% federal tax bracket. They decide to convert $50,000 from a traditional TSP to a Roth IRA.

Here’s a quick look at the math:

- Original Taxable Income: $190,000

- TSP Conversion Amount: +$50,000

- New Taxable Income: $240,000

That $50,000 bump pushes a big chunk of their income into the next tax bracket. For 2024, the 24% bracket for their filing status kicks in at $201,051. Their new income of $240,000 means a significant portion of that conversion gets taxed at the higher rate. The federal tax bill on just the converted amount comes out to roughly $11,800.

Don’t Forget About State Taxes

And the tax bite doesn't stop there. If you live in a state with an income tax, you can bet they’ll want their piece of the pie, too.

Let's say our example couple lives somewhere with a 5% flat state income tax. That’s another $2,500 added to their bill ($50,000 x 5%). Now, the total tax hit for their conversion is around $14,300. This is why you must have a plan to pay these taxes, ideally with money from a non-retirement account.

The Hidden Tax Trap for High Earners: NIIT

For those with higher incomes, there's another potential tax to watch out for: the Net Investment Income Tax (NIIT). This is a 3.8% tax that applies to certain investment income once your income crosses specific thresholds.

A Roth conversion boosts your modified adjusted gross income (MAGI). For high earners, this increase could trigger the 3.8% NIIT on either your net investment income or the amount your MAGI is over the threshold (which is $250,000 for married couples filing jointly), whichever is less. You can find more details about the Roth IRA conversion tax impact on Fidelity.com.

This can be a really expensive surprise. A large conversion that pushes your MAGI over the line could suddenly subject your other investment income—dividends, capital gains, interest—to this extra tax. It's a compounding effect that makes the true cost of your TSP conversion even higher. Calculating your potential MAGI beforehand is a critical step to avoid walking right into this tax trap.

Making the Move: A Step-by-Step Guide to Your TSP Rollover

Now that you understand the tax side of things, it’s time to get into the nitty-gritty of the transfer itself. Moving your TSP funds isn't complicated, but it does require careful attention to detail. Getting it right means your money moves smoothly, avoiding costly mistakes that could mess with your retirement goals.

The very first move is to give your money a new home. You can't just tell the TSP to send a check into the ether; you need to have a Roth IRA already set up and waiting at a brokerage firm.

Where Should Your Money Go? Choosing the Right Brokerage

This decision is more important than you might realize. Sure, plenty of big-name firms offer Roth IRAs, but they're not all the same. You're looking for a partner that fits your investment approach, your budget, and how much hand-holding you want.

When you're shopping around, zero in on these three things:

- Investment Options: This is a huge reason to leave the TSP in the first place. Make sure the brokerage gives you access to a wide universe of stocks, bonds, ETFs, and mutual funds. You need options to build the diversified portfolio you have in mind.

- Fees and Commissions: Keep an eye out for providers with low (or zero) account fees and commission-free trades for the investments you plan to use. High fees are like a slow leak in your retirement boat—they can seriously drag down your returns over the long haul.

- Customer Support and Tools: Good help is priceless, especially when you're moving a large sum of money. See if they have people who specialize in rollovers. Also, play around with their website and trading platform. Is it easy to use? Do their research tools give you the information you need to feel confident?

Once you’ve picked your brokerage and opened the Roth IRA, you'll get an account number. That number is the golden ticket—it's what you'll give the TSP to tell them exactly where to send your funds.

Direct vs. Indirect Rollovers: One Right Way and One Risky Way

Okay, it's time to actually start the transfer from your TSP account. You have two ways to get it done: a direct rollover or an indirect rollover. The one you choose has massive tax implications, and frankly, one option is vastly superior.

A direct rollover is the gold standard. The TSP sends your money straight to your new Roth IRA provider without you ever touching it. Your funds never hit your personal bank account, which keeps the whole transaction clean and simple for the IRS.

An indirect rollover, however, is playing with fire. With this method, the TSP cuts a check made out to you. The second you get that check, a 60-day countdown begins. You have exactly two months to deposit that money into your Roth IRA.

My Strong Advice: Go with a direct rollover. Every single time. It completely removes the risk of blowing the 60-day deadline and, crucially, it sidesteps mandatory tax withholding.

If you opt for an indirect rollover, the TSP is legally required to withhold 20% of your money for federal taxes right off the top. So, if you're rolling over $100,000, you’ll get a check for just $80,000. But here's the kicker: to complete the rollover properly, you still have to deposit the full $100,000 into your Roth IRA. That means you have to magically come up with that missing $20,000 out of your own pocket.

Sure, you’ll get that $20,000 back when you file your taxes next year, but it creates a massive and totally unnecessary cash-flow headache. For a full breakdown of the process, you can read our complete guide on how to rollover your TSP to an IRA for more detailed guidance.

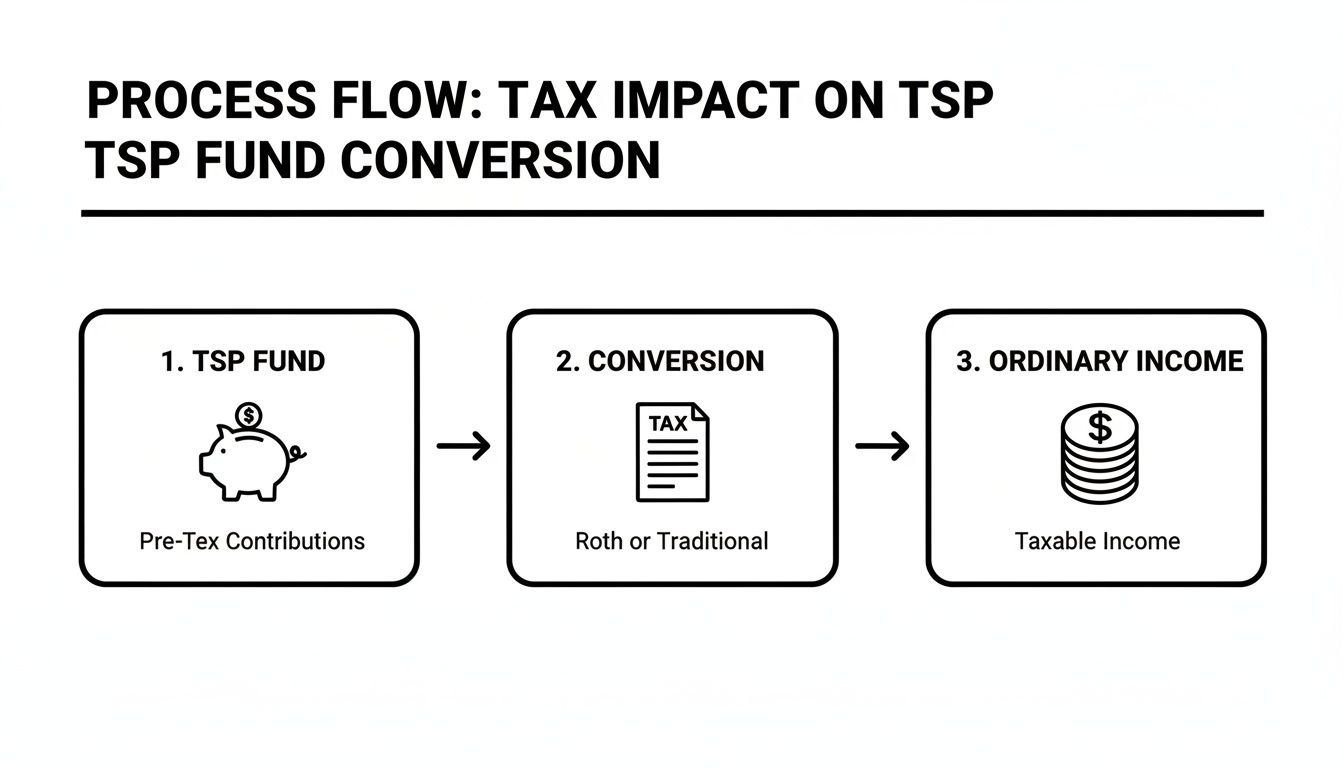

This diagram really clarifies how a transfer from a traditional TSP to a Roth IRA becomes a taxable event.

As you can see, the money you convert gets added directly to your ordinary income for the year, which is precisely why planning this move is so important.

The Paperwork and Timeline: What to Expect

It wasn't that long ago that you had to mail in a physical TSP-60 form to get this done. Thankfully, things are much easier now. The entire process can be kicked off right from your online TSP account.

Once you log in, find the withdrawals section and tell the system you want to do a rollover to an IRA. This is where you'll plug in the details for your new Roth IRA, including that account number and your brokerage's name and address. The online tool will walk you through it, making sure you select the direct rollover option.

Now, just be ready to wait a bit. After you hit submit, it can take the TSP a few weeks to process everything, sell your funds, and send the money on its way. I tell my clients to expect the entire process to take two to four weeks. Remember, during that time your money is out of the market. It’s probably not the best idea to start a transfer in the middle of a wild week on Wall Street. A little patience goes a long way toward a stress-free rollover.

Smart Strategies for Your TSP Conversion

Getting your money out of the TSP and into a Roth IRA is one thing. Doing it smartly is another game entirely.

A full, one-time conversion can be a blunt instrument. It often creates a massive—and frankly, unnecessary—tax bill that can derail your financial plans. The key is to stop thinking of the conversion as a single event. Instead, treat it as a multi-year strategy designed to systematically minimize your tax hit while maximizing your long-term, tax-free growth.

The whole point is to move your traditional TSP funds into a Roth IRA without sending your income skyrocketing into a much higher tax bracket in any single year. This requires a bit more finesse than just moving the entire balance at once.

The Power of Partial Conversions

Instead of a single, massive conversion, the smarter move is often to break it up into smaller, more manageable chunks over several years. This technique is what many financial planners call a Roth conversion ladder.

By converting just a portion of your TSP each year, you can strategically "fill up" your current tax bracket without spilling over into a more expensive one.

Think of your tax bracket as a bucket. A full conversion might overflow that bucket, forcing you to pay a much higher rate on every dollar that spills over. Partial conversions, on the other hand, let you add just enough each year to fill the bucket right to the brim, ensuring you don't waste a drop to a higher tax rate.

This method gives you incredible control over your taxable income from year to year. You can fine-tune the amount you convert based on your financial picture, creating a predictable and manageable tax obligation over time.

A Real-World Conversion Ladder Scenario

Let's walk through a practical example. Imagine a recently retired federal employee named Sarah. She's sitting on a $700,000 traditional TSP balance.

If Sarah converted the entire amount at once, she would create an enormous income spike. This would almost certainly push her into the highest federal tax brackets and could even trigger other unwanted taxes. It would be a tax nightmare.

Instead, Sarah opts for a more strategic approach. She decides to convert $70,000 each year for the next ten years. She's carefully calculated this amount to keep her squarely within a comfortable tax bracket—most likely the 22% or 24% bracket—letting her avoid those much higher rates at the top.

By spreading the tax liability over a decade, Sarah methodically builds a substantial tax-free Roth IRA without ever enduring a catastrophic tax year. She's transformed a daunting, six-figure tax bill into a manageable annual expense.

This systematic strategy can pay off handsomely. Financial models show that converting $70,000 annually from a $700,000 account, starting at age 63, could grow a Roth IRA balance to nearly $937,000 within ten years, assuming an 8% annual growth rate. This approach not only tames the immediate tax impact but also builds a significant source of future tax-free income.

Mastering the Art of Timing

Beyond how much you convert, when you do it is just as critical. The absolute best time to move TSP funds to a Roth IRA is during years when your income is lower than usual. These "low-income" years are a golden opportunity.

Look for these prime moments to pull the trigger on a conversion:

- The "Gap Years": This is the sweet spot for many retirees—that period after you stop working but before you start taking Social Security or are forced to take required minimum distributions (RMDs). Your taxable income is naturally lower, creating more room in those lower tax brackets.

- A Low-Earning Year: Maybe you took a sabbatical, worked part-time, or had a temporary dip in income for some other reason. These lulls are perfect moments to execute a partial conversion at a bargain tax rate.

- Market Downturns: This one feels counterintuitive, but a stock market correction can be a silver lining for conversions. When your TSP account value is temporarily down, you're essentially converting "depressed" shares. This means you can move more shares from your TSP to your Roth IRA for the same tax cost. When the market inevitably recovers, all of that rebound growth happens inside your tax-free Roth account.

Timing your conversions to line up with these events lets you get the most bang for your tax buck. You end up paying less in taxes for the same amount of future tax-free growth.

Of course, this conversion strategy is just one piece of a much larger retirement puzzle. To truly get the most out of your nest egg, you need a solid investment plan driving it all. For more ideas, you can explore our guide on the top TSP investment strategies for federal employees. When you combine intelligent conversion timing with a sound investment approach, you can dramatically improve your entire retirement outlook.

Common Rollover Mistakes You Must Avoid

Knowing the right steps is only half the battle. When moving your TSP to a Roth IRA, sidestepping the potential landmines is just as important. A few simple errors can turn a brilliant strategy into a costly mess, triggering unexpected tax bills and penalties that eat into your hard-earned retirement savings.

Think of it this way: a successful transfer is about more than just filling out paperwork. It's about being prepared for the details that can trip you up.

The Perils of an Indirect Rollover

This is, without a doubt, the single most dangerous mistake you can make. The TSP gives you two options for moving your money: a direct rollover or an indirect one. The indirect route is a minefield.

Here's what happens: the TSP cuts you a check directly. Right away, you have two huge problems.

First, the TSP is legally required to withhold 20% of your money for federal taxes. So, if you’re moving $100,000, the check you get in the mail is only for $80,000. That creates an instant, and completely avoidable, cash flow headache.

Second, a ticking clock starts the moment you receive the funds. You have exactly 60 days to deposit the full rollover amount into your Roth IRA. That means you have to find that missing $20,000 somewhere else to make the deposit whole. If you miss the 60-day window, the entire $100,000 is treated as a taxable distribution. And if you’re under 59 ½, you’ll get slammed with an extra 10% early withdrawal penalty.

A direct rollover is the only way to go. The TSP sends the funds straight to your new IRA provider. This move completely sidesteps the 20% withholding and eliminates the 60-day deadline drama. It’s safer, cleaner, and the only sensible choice.

Underestimating the True Tax Cost

A Roth conversion is a taxable event, and you need to pay those taxes with money from outside your retirement accounts. A surprisingly common error is failing to budget for that tax bill. People get caught off guard and end up raiding their newly converted Roth funds to pay the IRS.

This is a terrible move for two big reasons:

- It Defeats the Purpose: You’re pulling money out of the very account you wanted to grow tax-free, which shrinks the long-term benefit of the conversion in the first place.

- It Triggers More Penalties: That withdrawal could be an unqualified distribution, sticking you with more taxes and penalties on the money you just pulled out.

Before you even start the process, run the numbers. Calculate your estimated federal and state tax liability and stash that cash in a separate savings account. When tax day comes, the money will be waiting.

Navigating the Complex Pro-Rata Rule

The pro-rata rule often trips people up, especially feds who have both traditional (pre-tax) and Roth (after-tax) money in their TSP. The IRS won't let you pick and choose—you can't just convert the pre-tax portion.

Any withdrawal or rollover you take must be pulled proportionally from your traditional and Roth balances.

Let’s look at a quick example:

- Total TSP Balance: $500,000

- Traditional Balance: $400,000 (80% of total)

- Roth Balance: $100,000 (20% of total)

Say you want to roll over $50,000 to a Roth IRA. You don't get to decide where that money comes from. The TSP will automatically split the distribution: $40,000 (80%) will come from your traditional balance and be fully taxable, while $10,000 (20%) will come from your Roth balance and transfer tax-free.

If you ignore this rule, you could end up with a much larger tax bill than you planned for. When you have mixed funds, careful planning is non-negotiable.

Your Top TSP Transfer Questions, Answered

Planning a big financial move like this always brings up specific questions. It's totally normal. The details really matter, and getting clear answers is what gives you the confidence to pull the trigger.

Here are some of the most common questions we hear from federal employees wrestling with the TSP-to-Roth IRA decision.

Can I Transfer Funds From My Roth TSP to a Roth IRA?

Yes, absolutely. This is probably the cleanest, most straightforward move you can make. Since your Roth TSP was funded with after-tax money, rolling it over to a Roth IRA is a non-taxable event. The IRS has already gotten its cut, so there's nothing new to tax.

This is a really popular move for feds looking to consolidate their accounts or get access to a wider world of investment choices than the TSP offers. It’s a simple, direct, tax-free rollover.

Do I Have to Transfer My Entire TSP Balance at Once?

Not at all. In fact, for many people, moving everything at once would be a big mistake. You have the flexibility to do a partial transfer, and this is often the smartest way to go.

By transferring smaller chunks of your Traditional TSP balance over several years—a strategy known as a Roth conversion ladder—you can keep a tight rein on the tax bill each year. It’s all about avoiding that one massive transfer that could bump you into a much higher tax bracket.

This approach lets you methodically convert your pre-tax money into a Roth IRA, turning one giant tax headache into a series of small, manageable payments.

What Happens If I'm Still a Federal Employee?

This is a big one. As a general rule, if you’re still working for the government and are under age 59 ½, your TSP funds are locked down. You can’t move money out until you meet specific criteria.

The game changes once you hit 59 ½. At that point, you might qualify for an "age-based in-service withdrawal." This lets you roll over some or all of your vested balance while you’re still on the job. But for most people, the door for a full, no-strings-attached rollover swings wide open once they separate from federal service.

What Are the Reasons to Keep My Money in the TSP?

Moving to an IRA gives you more flexibility, no doubt. But don't overlook the unique perks of the TSP. It has some powerful advantages that are tough, if not impossible, to find anywhere else.

Here's why you might want to leave at least some of your money right where it is:

- Rock-Bottom Fees: The TSP’s expense ratios are legendarily low. They are often drastically cheaper than what you'll find in commercially available IRAs, which means more of your money stays invested and working for you.

- The One-of-a-Kind G Fund: This is the TSP’s secret weapon. It offers complete principal protection backed by the U.S. government while paying an interest rate tied to government securities. You simply cannot find this combination of safety and return in the private market.

- Serious Creditor Protection: Your TSP assets are shielded by strong federal laws. In many cases, this protection is far more robust than the state-level laws that govern most IRAs, offering a better shield against lawsuits.

Navigating these decisions is what a solid retirement plan is all about. At Federal Benefits Sherpa, we live and breathe this stuff. We help federal employees make sense of these complex choices every single day. A free 15-minute benefits review can give you the personalized clarity you need to move forward with confidence. Book your complimentary session with Federal Benefits Sherpa today.