A Guide to Your TSP Withdrawal Options in Retirement

Figuring out what to do with your Thrift Savings Plan is easily one of the most important financial decisions you'll ever make. This guide is your roadmap to understanding all the TSP withdrawal options out there, breaking down the complex rules into simple, practical advice. We’ll look at how choosing between installments, a lump sum, or a rollover will directly impact your retirement income for decades.

Charting Your Course for TSP Withdrawals

Think of your TSP account like a financial reservoir you’ve spent your entire career filling up, drop by drop. Now that you're getting close to retirement, it's time to decide how to open the tap. These choices aren't just about getting your money out; they're about designing an income stream that will support the life you want to live.

Thankfully, the TSP Modernization Act threw out the old, rigid "one-and-done" withdrawal system. Today, you have a lot more flexibility and a much bigger toolkit to work with. The first step to building a solid retirement plan is simply understanding what those tools are and how they work.

This guide will walk you through everything, covering:

- The main ways to get your money out after you leave federal service.

- The specific rules and, importantly, the tax consequences for each choice.

- A simple framework to help you match your withdrawal strategy to your personal goals.

The real goal here isn't just to list your options. It's to help you feel confident picking the right options for your specific situation, so you can shift from saving money to creating a reliable income with total clarity.

To get started, let's look at a quick summary of the main withdrawal paths available once you've separated. This table gives you a bird's-eye view before we dig into the details of each one.

Quick Summary of Post-Separation TSP Withdrawal Options

| Withdrawal Option | Best For | Key Feature |

|---|---|---|

| Lump-Sum Withdrawal | Immediate, large financial needs like paying off a mortgage or a major purchase. | Taking your entire account balance in a single payment, offering maximum immediate liquidity. |

| Installment Payments | Creating a predictable, customized income stream similar to a personal paycheck. | Receiving regular payments (monthly, quarterly, or annually) of a specific dollar amount. |

| TSP Life Annuity | Those seeking maximum security and a guaranteed income that cannot be outlived. | Using your TSP balance to purchase a lifetime monthly payment from a private insurance provider. |

| Rollover to an IRA | Gaining access to a wider range of investment choices and more withdrawal flexibility. | Moving your TSP funds to an Individual Retirement Account (IRA) that you control. |

Now that you have the basic landscape, let's explore what each of these options really means for you and your money.

The Core TSP Withdrawal Choices After Separation

Once you hang up your federal hat for the last time, your Thrift Savings Plan account transforms. It’s no longer just a savings account; it's the bedrock of your retirement income. Figuring out how to draw from that hard-earned money is one of the biggest financial decisions you'll ever make. Let's walk through your main options.

Think of it like this: you've spent decades earning a prize. Now, you get to decide how to collect it. You can grab the whole prize at once, arrange for a series of payouts, or trade it in for a guaranteed income that lasts a lifetime. Each path has its own set of pros and cons, and the right one for you depends entirely on your vision for retirement.

Option 1: The Lump-Sum Withdrawal

A lump-sum withdrawal is exactly what it sounds like—you pull your entire TSP balance out in one single payment. It's the financial equivalent of hitting a jackpot and taking the cash option. This gives you immediate access to all your money, which can be perfect for big-ticket items like paying off your mortgage or buying that dream retirement RV.

But hold on, because this move has some serious strings attached. A huge withdrawal can easily catapult you into a much higher tax bracket for that year, meaning a hefty chunk goes straight to Uncle Sam. Once you take a full lump sum, that money is no longer invested in the low-cost TSP funds, and it's entirely on you to make it last for the rest of your life.

Option 2: Installment Payments

This is my personal favorite for most people. Installment payments are like setting up your own customized paycheck from your TSP. You get to decide on a specific dollar amount and a schedule—monthly, quarterly, or annually. It's easily one of the most flexible TSP withdrawal options you have.

This approach gives you a fantastic blend of control and predictability.

- Flexibility: You can start, stop, or tweak the payment amount whenever you need to.

- Continued Growth: The rest of your TSP balance stays right where it is, invested and continuing to grow based on your fund choices.

- Reliable Income: It creates a steady, predictable income stream to supplement your FERS pension and Social Security, covering your day-to-day bills.

This strategy lets you have your cake and eat it too. You get the cash flow you need while the bulk of your nest egg keeps working for you.

One of the smartest things about installment payments is how they help you manage taxes. By taking smaller, regular withdrawals, you can often keep yourself in a lower tax bracket compared to the massive tax hit from a lump sum.

Option 3: The TSP Life Annuity

Your third choice is to use some or all of your TSP balance to purchase a life annuity. Essentially, you're trading a chunk of your account balance for a guaranteed, lifelong pension paid by a private insurance company. The TSP handles the transaction, but once you make this choice, it’s pretty much set in stone.

An annuity offers incredible peace of mind if your biggest fear is outliving your savings. It completely removes market risk from the equation for that portion of your money. You're guaranteed to get a check every single month for the rest of your life, no matter what the stock market does or how long you live.

You can customize it a bit:

- Single Life: This gives you the highest possible monthly payment, but it stops when you pass away.

- Survivor Benefit: The monthly payment is a little smaller, but it continues to pay out to your spouse or another beneficiary after your death.

The major downside here is the loss of control. The money you use for the annuity is no longer yours to manage, invest, or leave to your kids, other than any survivor benefit you've built in.

Understanding Required Minimum Distributions (RMDs)

No matter which path you take, you'll eventually run into Required Minimum Distributions (RMDs). This is the IRS's way of making sure they eventually get to tax the money in your traditional TSP. Once you reach a certain age (currently 73 for most people), the government requires you to start taking withdrawals.

The TSP Modernization Act, which kicked in on September 15, 2019, was a game-changer here. Before the act, retirees hitting age 70½ were forced to make a permanent, all-or-nothing withdrawal decision. It was a stressful deadline.

Now, things are much more flexible. If you haven't started withdrawals by your RMD age, the TSP will simply calculate the minimum amount you're required to take and send it to you automatically each year. This is a huge relief, as it prevents you from being pushed into a hasty decision just to beat a deadline. You can dig into the specifics by checking out the official withdrawals process updates from the Department of Labor.

Understanding Rollovers and In-Service Withdrawals

Beyond the usual withdrawal choices you face after leaving federal service, there are a couple of other powerful options in your TSP toolkit. These two strategies solve very different problems. One is all about moving your money for more investment freedom, while the other acts as a financial safety valve if you need funds while still on the job.

Let's start with rollovers—think of it as changing the address for your retirement savings. Then, we'll dive into the specifics of in-service withdrawals, which let you tap into your TSP under certain circumstances without having to quit your job.

Moving Your Money with a Rollover

A rollover isn't really a "withdrawal" in the traditional sense; it's a transfer. You're simply moving your TSP balance from one qualified retirement account to another, most often an Individual Retirement Account (IRA). The beauty of this is that your money stays in its tax-advantaged bubble, letting you sidestep the immediate tax bill you’d get from cashing out.

So, why would anyone bother? The main driver is a desire for more control and a much bigger investment playground. The TSP is famous for its rock-bottom fees and simplicity, but let's be honest—its investment menu is pretty limited with just a handful of core funds.

Rolling your funds over to an IRA blows the doors wide open to a huge universe of investment choices:

- Individual Stocks and Bonds: You can invest directly in your favorite companies or buy government and corporate debt.

- Mutual Funds and ETFs: This gives you access to thousands of funds that cover every possible market sector, industry, and investment strategy you can imagine.

- Real Estate Investment Trusts (REITs): Want to get into the real estate market without the headache of being a landlord? REITs are your answer.

For a savvy investor, this kind of flexibility is a game-changer. But this freedom isn't free. It comes with the responsibility of managing a more complex portfolio and, often, higher management fees than the TSP. If this sounds like a path you want to explore, it's critical to know exactly what you're doing. Our detailed guide offers a complete walkthrough of how to rollover your TSP to an IRA.

Accessing Funds While Still Employed

What if you have a pressing need for cash but you're years away from retirement? That's where in-service withdrawals come in. These options are designed for very specific situations and are governed by strict rules meant to keep people from raiding their retirement nest eggs too early.

There are two primary types of in-service withdrawals you can take as a current federal employee.

Age-Based Withdrawals

Once you hit age 59½, you unlock the ability to take what's called an age-based "in-service" withdrawal. This lets you access your vested TSP account balance without having to prove any sort of financial hardship. You're allowed to take up to four of these withdrawals per calendar year, but remember, the money you take out is taxed as ordinary income.

Think of this as a pre-retirement trial run. It lets you tap into your savings once you've hit a key retirement milestone, giving you a way to fund a big project or just supplement your income without having to leave your career.

Financial Hardship Withdrawals

This option should be treated as a true last resort, reserved for only the most dire financial emergencies. The TSP is very clear about what qualifies as a hardship—things like recurring negative cash flow, medical bills not covered by insurance, or legal fees from a divorce.

You have to prove your need and show you've exhausted other financial resources first. A hardship withdrawal is a permanent hit to your retirement savings and can seriously jeopardize your long-term financial security. Unfortunately, recent data shows a worrying trend here. The 2024 Annual Report from the FRTIB noted that hardship withdrawals increased to 3.9% of participants, with the second-lowest paid group showing the highest withdrawal rate at 8.47%. You can dig into more of these trends in the official TSP annual report.

Key Financial Rules and Tax Implications

Knowing your TSP withdrawal options is just one piece of the puzzle. The other, arguably more important piece, is understanding the financial rules that govern those options.

Think of these rules as the guardrails on your retirement highway. They're not suggestions—they're what keep your hard-earned savings safe and ensure you get to keep as much of it as legally possible. Let's break down the two most critical concepts you need to master: taxes and penalties.

Every dollar you pull from your Traditional TSP is treated as ordinary income. That’s right, the IRS sees it the same way it saw your federal salary, and it gets taxed at your regular income tax rate. A large one-time withdrawal can easily bump you into a higher tax bracket for the year, leading to a much bigger tax bill than you anticipated.

On the flip side, qualified withdrawals from your Roth TSP are completely tax-free. This is because you already paid the taxes on that money when you contributed it. To be considered "qualified," two conditions must be met: you have to be at least 59½ years old, and at least five years must have passed since January 1st of the year you made your very first Roth contribution.

The Pro-Rata Rule Explained

One of the most common points of confusion for federal employees is the pro-rata rule. Simply put, you can't pick and choose which TSP fund to withdraw money from. You can't, for example, decide to sell off your C Fund holdings to lock in some gains while leaving your G Fund untouched.

Imagine your TSP account is a big fruit smoothie blended from five ingredients: grapes (G Fund), cherries (C Fund), strawberries (S Fund), kiwis (I Fund), and figs (F Fund). When you pour a glass, you get a bit of everything in the same proportion as the original blend. You can't just pour out the cherry flavor. If 40% of your smoothie is cherry, then 40% of what's in your glass will be cherry.

This rule is in place to maintain your chosen asset allocation. It stops you from trying to time the market by cherry-picking funds, making sure your withdrawal reflects your overall investment strategy.

This proportional system applies to every single withdrawal you make, whether it’s a one-time partial withdrawal, a series of installment payments, or even a Required Minimum Distribution (RMD).

Navigating the Early Withdrawal Penalty

Generally, the IRS slaps a 10% early withdrawal penalty on money taken from retirement plans like the TSP before you turn 59½. This stings because it’s on top of the regular income taxes you'll owe. It's a hefty penalty designed to keep people from raiding their retirement accounts too early.

But here’s some good news for federal employees. There are special exceptions that can help you sidestep this penalty. A big one is this: if you separate from federal service in the year you turn 55 or later, you can take withdrawals from your TSP without that 10% penalty. This is a huge advantage for feds planning an early retirement. You can dive deeper into this by reading our complete guide to early TSP withdrawals.

The TSP has some hard numbers you need to know. For instance, any partial withdrawal must be for a minimum of $1,000. And that 10% IRS penalty is a critical number to plan around unless you qualify for an exception. You can see how these rules work in the government’s official guidance and find more great insights about TSP loans and savings rates on GovExec.

Quick Reference for Taxes and Penalties

To pull all these complex rules together, I've created a simple table summarizing how different withdrawal scenarios are usually handled. It breaks down the tax and penalty implications for both your Traditional and Roth TSP balances.

TSP Withdrawal Tax and Penalty Quick Reference

A summary of the primary tax and penalty rules associated with different TSP withdrawal scenarios.

| Withdrawal Type | Federal Tax Treatment (Traditional TSP) | Federal Tax Treatment (Roth TSP) | 10% Early Withdrawal Penalty? |

|---|---|---|---|

| Post-Separation (Age 59½+) | Taxed as ordinary income | Tax-free (if qualified) | No |

| In-Service (Age 59½+) | Taxed as ordinary income | Tax-free (if qualified) | No |

| Separated (Age 55-59½) | Taxed as ordinary income | Tax-free (if qualified) | No, if separated in the year you turn 55 or later |

| Separated (Under Age 55) | Taxed as ordinary income | Earnings taxed + 10% penalty | Yes, unless another exception applies |

| Hardship (While Employed) | Taxed as ordinary income | Earnings taxed + 10% penalty | Yes, unless another exception applies |

| Rollover to IRA | Not taxed at time of rollover | Not taxed at time of rollover | No |

Getting a firm grip on these financial rules is non-negotiable before you make a move with your TSP. One small misstep could lead to a surprisingly large tax bill or unnecessary penalties, eating into the retirement nest egg you worked so hard to build.

How to Choose the Right Withdrawal Strategy

Alright, let's move from theory to reality. Picking the right TSP withdrawal options isn't about finding some secret, one-size-fits-all answer. It's about crafting a strategy that fits your life, your financial situation, and your vision for retirement.

To get there, you have to ask yourself some serious questions. These go deeper than just crunching numbers; they get to the very heart of what you want your post-federal career life to look like. Think of your answers as a compass—they’ll point you toward the withdrawal path that makes the most sense for you.

Key Questions to Guide Your Decision

It's time for an honest look at your personal circumstances. Remember, your FERS pension and Social Security are the bedrock of your retirement income. Your TSP is the powerful, flexible tool you get to control.

- What do you actually need to live on? Don't just guess. Sit down and map out a real retirement budget. Tally up the essentials like housing and healthcare, but don't forget the fun stuff like travel, hobbies, and spoiling the grandkids. This number tells you exactly how much work your TSP needs to do each month or year.

- How much risk can you stomach? If a nosedive in the stock market would have you tossing and turning all night, then a strategy built on security, like an annuity, might be your best friend. But if you're okay with some market bumps for a shot at better long-term growth, then keeping your money invested and taking installment payments could be a much better fit.

- What do you want to leave behind? Is passing on a financial legacy to your kids or a favorite charity a big deal for you? If so, you need to be careful. Some options, like a single-life annuity, won't align with that goal because the insurance company keeps what's left, not your heirs.

- Are there any big-ticket expenses on the horizon? Maybe you’re dreaming of a mountain cabin or planning to help with a grandchild's college tuition. A partial lump-sum withdrawal or the flexibility of an IRA rollover could give you the cash you need for those major life moments.

Answering these questions gives you the personal data you need to build a strategy that feels right, one that strikes the perfect balance between security and freedom.

Comparing Different Retirement Personas

To really see how this plays out, let's look at a couple of common scenarios I see with federal retirees. Their priorities are totally different, which leads them to completely different—but equally smart—TSP strategies.

Persona 1: "Steady-Income Steve"

Steve is 62, and his number one priority is security. He wants a rock-solid, predictable income stream that he and his wife can count on for the rest of their lives. He decides to use a chunk of his TSP to buy a joint-life annuity, which guarantees a monthly check as long as either of them is alive. For everything else, he keeps the rest of his TSP in the G Fund and sets up small monthly installment payments to cover his fun money.

Persona 2: "Flexible-Fiona"

Fiona is 65, and for her, it's all about control and growth potential. She rolls her entire TSP balance over into an IRA. This move blows the doors open to a much wider universe of investment choices, allowing her to fine-tune her portfolio. She manages her own withdrawals, taking more in years when she wants to travel the world and pulling back in other years to keep her tax bill down.

These examples make it crystal clear: there is no single "right" way to do this. The best strategy is the one that supports your personal definition of a great retirement. Your plan should be as unique as your federal career.

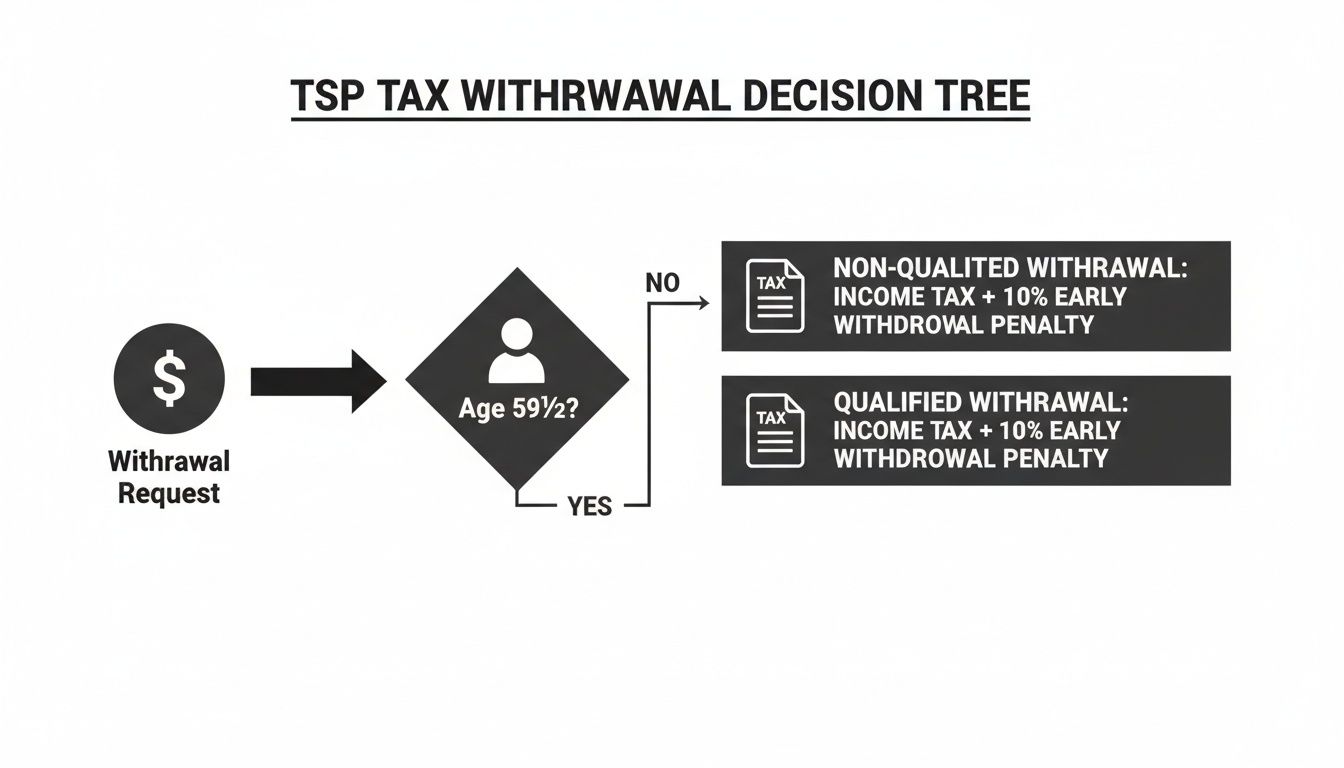

This decision tree gives you a great visual for how your age is the main factor in the tax rules for your withdrawals.

As the chart shows, hitting age 59½ is the magic number for avoiding that painful 10% early withdrawal penalty on your distributions.

Just remember that while in-service withdrawals are on the table, they’re a different beast than the strategies you’ll use after you separate. Sometimes, a simple TSP loan is a much smarter move for short-term cash needs. For a deep dive on that topic, check out our guide to borrowing from your TSP.

Thinking through these factors carefully is what will empower you to build a withdrawal plan that delivers both financial security and, just as importantly, total peace of mind.

Your Next Steps and Getting Expert Guidance

Wading through all the TSP withdrawal options is a big job. Making the right call is absolutely critical for locking in a secure and comfortable retirement. By now, you've got a detailed map of the territory—from taking a single lump-sum payout to setting up flexible installments, rolling funds over, or buying a life annuity. Each path has its own unique set of pros and cons.

Your next mission is to turn all this knowledge into a real-world action plan. The decisions you make right now will directly shape your financial reality for decades, affecting everything from your monthly cash flow to how much you'll owe in taxes. It’s all about building a solid bridge from your working years to a future where your money is finally working for you.

Creating Your Personal Withdrawal Blueprint

While this guide gives you a solid foundation, your situation is yours alone. A strategy that’s a perfect fit for one federal employee might be a terrible idea for another. This is where the real work begins—applying these concepts to your own life and goals.

First things first, you need to get your financial documents in order.

- Review Your TSP Statement: Get a crystal-clear picture of your current balance, paying close attention to the split between your Traditional and Roth accounts.

- Estimate Your Retirement Budget: Figure out your essential living expenses and then add in your wish list for travel, hobbies, and other fun stuff.

- Project Your Other Income: Don't forget to factor in your FERS pension and estimated Social Security benefits. This will show you exactly how much of an income gap your TSP needs to fill.

Remember, the goal isn't just to get your hands on your money. It's to create a sustainable income stream that will last for the rest of your life. Your TSP is a powerful tool, but it's designed to work hand-in-hand with your other federal benefits, not in isolation.

The Value of a Professional Guide

Feeling a little overwhelmed by it all? That’s completely normal. These are big decisions with permanent consequences. While you can certainly navigate this on your own, partnering with a professional who specializes in federal benefits can bring a level of clarity and confidence that’s hard to achieve alone.

Think of it this way: you wouldn't try to perform surgery on yourself after reading a medical textbook. In the same way, designing a retirement income plan that needs to last for 30 years or more often benefits from an expert’s touch. A specialist can help you pressure-test your plan against things like market downturns, rising inflation, and whatever unexpected curveballs life decides to throw your way.

At Federal Benefits Sherpa, we live and breathe this stuff. Our entire focus is on helping federal employees just like you build retirement strategies that are built to last. We can help you put together a custom withdrawal plan that lines up perfectly with your goals, ensuring your financial future isn't just planned, but truly secured.

Your Top TSP Withdrawal Questions Answered

When you're getting close to retirement, the what-ifs start popping up. It's completely normal. Let's tackle some of the most common questions federal employees ask about getting their money out of the Thrift Savings Plan.

Can I Change My Mind on My Withdrawal Choice?

This is a big one, and the answer is a classic "it depends." The flexibility you have is directly tied to the withdrawal method you pick from the get-go.

If you opt for installment payments, you're in the driver's seat. You can change the dollar amount, switch from monthly to quarterly or annual payments, or even stop them entirely whenever you want. It’s a great way to adjust your income stream as life in retirement unfolds.

On the other hand, choosing a life annuity is a permanent decision. Once you use your TSP funds to buy that annuity contract, the deal is done. You can't alter the payments or access the lump sum again. You're trading flexibility for the security of a guaranteed income for life.

How Will My TSP Withdrawals Impact My Social Security?

It’s easy to forget that these two benefits don't exist in a vacuum—they can definitely affect each other, especially when it comes to taxes. The IRS calculates your "combined income" to determine if your Social Security benefits are taxable. This formula includes your adjusted gross income, any nontaxable interest, and, crucially, 50% of your Social Security benefits.

Taking a large lump-sum or hefty installment payments from your Traditional TSP can really inflate that combined income number. If it pushes you over certain IRS thresholds, as much as 85% of your Social Security benefits could suddenly become taxable.

Think of it this way: your TSP withdrawals can turn up the tax dial on your Social Security. A smart strategy often involves spreading out your TSP income over several years to stay under those tax-triggering income levels.

What if I Leave My Federal Job but Don't Touch My TSP?

Good news: you don't have to do anything with your TSP account the day you separate from service. In fact, just letting it sit can be a powerful move.

Your money stays invested in the TSP's famously low-cost funds, where it can continue to grow. You still have full access to manage your investments online, shifting between funds as you see fit. If you don't need the cash right away, leaving it in the plan to keep growing is often the best course of action.

Of course, you can't leave it there forever. The IRS will eventually require you to start taking money out through Required Minimum Distributions (RMDs), which currently begin at age 73. If you haven't started withdrawals by then, the TSP will automatically calculate your RMD and send it to you each year to stay compliant.

Making these decisions can feel overwhelming, but you don't have to do it alone. At Federal Benefits Sherpa, we help federal employees put all the pieces together—TSP, FERS, and Social Security—into a cohesive retirement plan. Schedule your free benefits review today to get started.