A Federal Employee's Guide to Open Season Federal Benefits

Each year, federal employees get one specific window of opportunity to make critical decisions about their benefits. This period, known as Federal Open Season, is your chance to enroll in or change your health, dental, and vision insurance plans. It's the most important time of the year to make sure your coverage truly fits your life and budget for the year ahead.

Your Annual Benefits Check-Up: Why Open Season Matters

Think of Open Season as the annual health and financial check-up for your benefits. It’s a dedicated period—usually running from mid-November to mid-December—where you get to actively manage some of the most important pieces of your compensation package. Simply letting your benefits auto-renew without a second thought is a classic mistake, like leaving old subscriptions running that you no longer use.

Being proactive here isn't just a good idea; it's a fundamental part of smart federal career management. Life happens. Maybe you got married, welcomed a new baby, or need to manage a new health condition. Your benefits need to keep up with those changes. This is your moment to ensure you're not overpaying for coverage you don’t need or, even worse, finding yourself underinsured when it matters most.

The Financial Stakes of Inaction

Ignoring Open Season isn't a passive act—it's a financial decision with very real consequences. Healthcare costs are always on the move, and the plan that was a great deal last year might be a poor value this year. Making the right adjustments can easily save you thousands of dollars in premiums and out-of-pocket expenses over the next 12 months.

Recent trends really drive this point home. For the 2026 plan year, the overall average premium increase for the Federal Employees Health Benefits (FEHB) program is a hefty 12.3%. That comes on the heels of a steep 13.5% jump in 2025. That’s a staggering cumulative increase of over 25% to your out-of-pocket premium costs in just two years.

The Core Programs in Play

During this time, you have direct control over the foundational programs in your benefits package. Each one is distinct, and a decision you make for one doesn't carry over to the others.

For a quick overview, here's a snapshot of what Open Season is all about.

Federal Open Season At a Glance

| Component | Description | Typical Timeframe |

|---|---|---|

| What It Is | The annual period for federal employees to review, enroll in, or change their health, dental, and vision insurance, and flexible spending accounts. | Mid-November to Mid-December |

| Who It's For | Most active federal employees, annuitants, and other eligible family members. | |

| Key Programs | FEHB (Health), FEDVIP (Dental/Vision), and FSAFEDS (Flexible Spending Accounts). |

This table highlights the essentials, but it's important to understand the specific programs you can adjust.

The main programs you can change during the open season federal benefits window are:

- Federal Employees Health Benefits (FEHB) Program: This is your core health insurance. You can switch plans, change your enrollment type (like moving from Self Only to Self and Family), or enroll for the first time if you're a new, eligible employee.

- Federal Employees Dental and Vision Insurance Program (FEDVIP): This is completely separate from your health plan and requires its own enrollment. You can pick from various dental and vision carriers to find the right fit for your family.

- Federal Flexible Spending Account Program (FSAFEDS): This lets you set aside pre-tax dollars for medical and dependent care costs. This is a big one: you must re-enroll in an FSA every single year to participate. Your enrollment does not automatically carry over.

By actively engaging with Open Season, you transform a routine administrative task into a powerful strategic opportunity. You are taking direct control of your financial health and ensuring your family's well-being is protected for the year ahead.

While the federal system has its own unique rules, the basic concept is similar to what's found in the private sector. If you want to understand the broader idea, you can learn more about What Is Open Enrollment For Health Insurance, which shares many of the same principles.

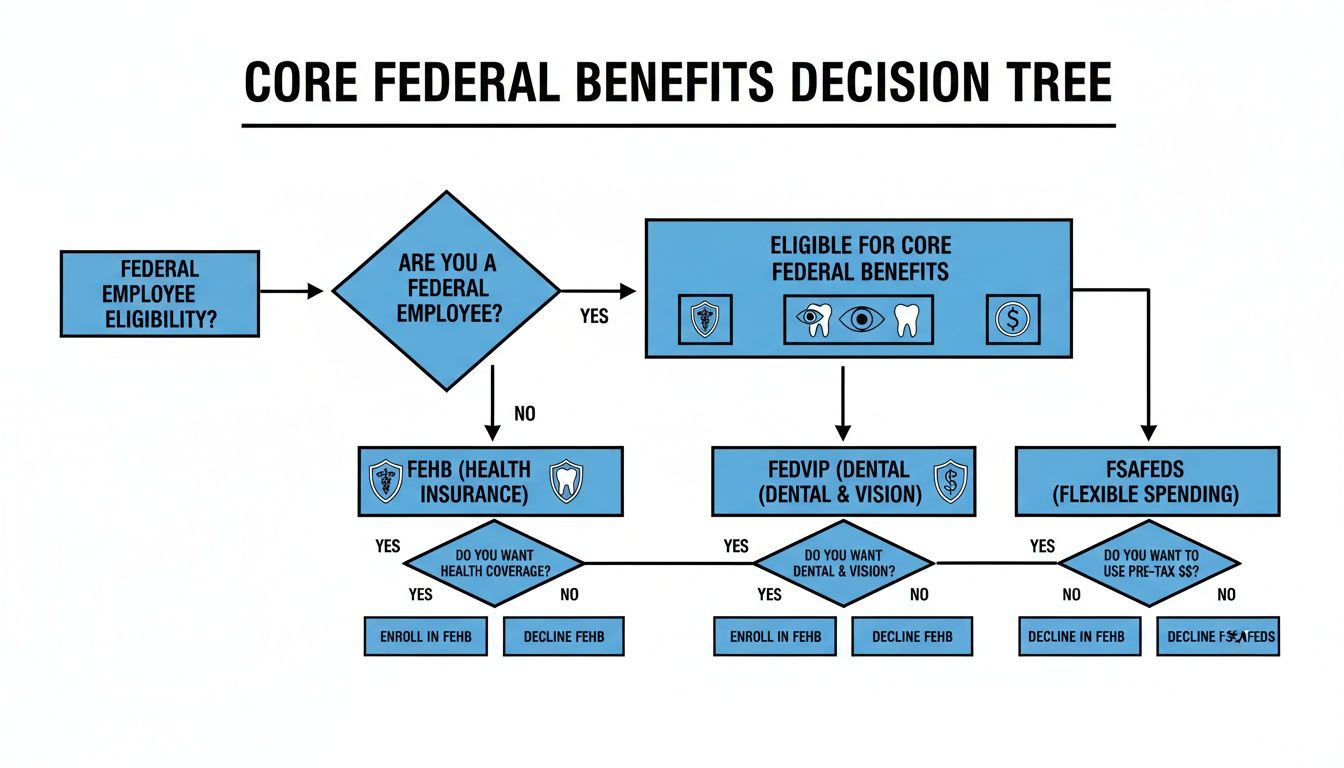

A Closer Look at Your Core Federal Benefits

Trying to make sense of federal benefits can feel like you're learning a new language, with a whole dictionary of acronyms and rules. During Open Season, it really boils down to making decisions on a few key programs. Let’s walk through exactly what they are and what you can do.

Think of these benefits as different tools in your financial toolkit. Each one has a specific job, and they don't just work together on their own. You have to decide which tools you need for the year ahead and how you're going to use them.

Your Health Insurance Foundation: FEHB

The Federal Employees Health Benefits (FEHB) Program is the bedrock of your coverage. This is your main medical insurance—the plan that covers everything from routine doctor’s visits to hospital stays. When it comes to Open Season, FEHB is where you have the most freedom to make changes.

Your decisions here go beyond just picking the plan with the lowest premium. You also have to choose the right enrollment type for your family's situation.

- Self Only: This covers just you, the federal employee. It’s the simplest and cheapest option, perfect if you're single and don't have any dependents.

- Self Plus One: This covers you and one eligible family member, like your spouse or a child. It's almost always a better deal than a family plan if you only need to insure one other person.

- Self and Family: This is the umbrella plan, covering you and all of your eligible family members. It’s the go-to choice for employees who need to cover a spouse and multiple children.

Choosing the right tier is a major financial decision. For example, if you just have one child to cover, a Self Plus One plan will save you money compared to the Self and Family option. You can dive deeper in our complete guide to the Federal Employees Health Benefits program FEHB.

Beyond the Basics: FEDVIP for Dental and Vision

Here’s something that trips people up all the time: dental and vision coverage are not part of your FEHB plan. The Federal Employees Dental and Vision Insurance Program (FEDVIP) is a completely separate program, and you have to enroll in it separately.

If you do nothing, you won't have federal dental or vision insurance. It’s that simple. You have to actively pick a FEDVIP plan during Open Season if you want this coverage. The good news is that there are tons of carriers to choose from, so you can find a plan that fits your specific needs, whether it's for routine cleanings, braces, or new glasses.

Tax-Smart Savings with FSAFEDS

The Federal Flexible Spending Account Program (FSAFEDS) is one of the most powerful tools you have, but it's also widely misunderstood. An FSA lets you put money aside from your paycheck before taxes to pay for out-of-pocket medical or dependent care costs.

And here’s the most important rule to remember: You must re-enroll in your FSA every single year. Your contributions from last year do not automatically roll over.

FSAFEDS is a "use-it-or-lose-it" account. You have to estimate your expenses for the coming year pretty carefully, because any money left over at the end of the year (beyond a small carryover amount) is forfeited.

For instance, if you know your child will need braces with a $3,000 out-of-pocket cost next year, putting that money into an FSA means you're paying for it with tax-free dollars. A little planning ahead gives you an automatic discount on those necessary expenses.

A Quick Note on FEGLI Life Insurance

While it’s not officially part of the annual open season federal benefits election period, now is the perfect time to review your life insurance. The Federal Employees' Group Life Insurance (FEGLI) program is pretty restrictive; you generally can’t make changes during Open Season without a Qualifying Life Event or passing a physical.

Still, think of Open Season as your annual reminder to check in on your life insurance needs. Has your family grown? Did you buy a house? Big life changes often mean your current FEGLI coverage might not be enough anymore. This is your chance to review your policy and decide if you need to look at other options to make sure your family is truly protected.

How to Choose the Right Benefits for Your Life Stage

Deciding on your benefits during Open Season can feel overwhelming. With so many options on the table, it's tempting to just zero in on the monthly premium. But the best choice for you and your family goes much deeper than that.

To really get this right, you have to look past the sticker price and weigh four key factors: your total potential costs, the level of coverage you actually need, access to your preferred doctors, and, most importantly, your current stage in life. This simple framework shifts your thinking from just picking a plan to strategically building the right protection.

This flowchart maps out the decision-making process, starting with your core health plan and flowing into your other benefit choices.

As you can see, your health plan (FEHB) is the foundation. Once that’s set, your decisions on dental, vision, and tax-advantaged accounts like FSAs become much clearer.

Scenarios For Early and Mid-Career Feds

Your benefit needs aren't static; they change right alongside your life and career. What works for a young, single employee is rarely the right fit for someone in mid-career raising a family.

Example: The New Hire Meet Sarah, a 28-year-old federal employee who's single and in great health. Her main focus is keeping her monthly expenses low so she can build her savings. A High Deductible Health Plan (HDHP) paired with a Health Savings Account (HSA) is likely her best bet. The lower premiums mean more money in her pocket each month, and the HSA gives her a fantastic, triple-tax-advantaged vehicle for saving—money she can use for future medical bills or even let grow for retirement.

Example: The Growing Family Now consider Mark, who is 45 with a spouse and two active teenagers. One of his kids is getting braces, and the other is a soccer player, which means an unexpected trip to urgent care is always a possibility. For his family, a traditional PPO or HMO with a low deductible and predictable copays offers peace of mind. The higher monthly premium is a worthwhile trade-off for financial stability and strong coverage, especially for the orthodontic work they’ll need through their FEDVIP plan.

Navigating Benefits Near Retirement

As retirement gets closer, your benefit choices carry even more weight. The decisions you make now can lock in your healthcare access and financial security for the rest of your life. Everyone knows about the "5-year rule" for keeping FEHB in retirement, but you also need to think about how your plan will work alongside Medicare down the road.

For pre-retirees, the conversation shifts from short-term savings to long-term value. You're looking for robust prescription drug coverage and a plan with a solid nationwide network, just in case you decide to travel or relocate. The lowest premium plan is rarely the wisest choice when you're planning for a fixed income in retirement.

Making the right call is more critical than ever, especially as costs are on the rise. We're seeing open season federal benefits premiums climb sharply. For 2026, FEHB premiums are projected to jump by an average of 12.3%, a rate that's leaving the private sector in the dust.

In fact, a recent survey showed that only 50% of federal employees plan on keeping their current health plan—a major drop from past years that signals widespread concern over value and affordability. You can see more on this in the official OPM open season highlights.

Your life stage is the most powerful filter for making benefit decisions. A plan that's ideal for a new employee could be financially risky for someone nearing retirement. Always match your coverage to where you are, not just what seems cheapest today.

Choosing the right benefits is about weaving a personalized safety net. When you take the time to analyze your real costs, coverage needs, and life stage, you can select plans that truly protect your health and support your financial goals, giving you genuine peace of mind for the year ahead.

Your Step-By-Step Open Season Action Plan

Navigating the annual open season for federal benefits can feel a bit like cramming for a final exam. To take the pressure off, I've laid out a simple, step-by-step checklist to get you through it. Think of this as your roadmap, guiding you from the initial review all the way to your final submission so you can feel confident in your choices.

This is your pre-flight check before your benefits take off for the year ahead. A little bit of prep work now can save you a whole lot of turbulence down the road. The idea is to move through it methodically, making sure no important details get missed.

Step 1: Gather Your Intelligence

Before you can even think about comparing plans, you need to get a clear snapshot of where you are now and what you'll need next year. This first step is all about gathering your information in one place. Don't be tempted to skip it—having these details at your fingertips will make everything else so much easier.

Here’s what your pre-analysis kit should include:

- Your Current Plan Details: Find your FEHB and FEDVIP plan codes and have a summary of your current benefits handy.

- List of Prescriptions: Jot down every single medication you and your family members take, including the specific dosages. This is absolutely critical for checking the drug formularies of any new plans.

- Your Doctor Roster: Make a list of all your go-to doctors, specialists, and hospitals. You'll need this to check if they are in-network for any plans you're considering.

- Anticipated Medical Needs: Take a moment to think about the year ahead. Are you planning for a surgery? Does a child need braces? Are you expecting a new addition to the family? These major life events will directly shape the kind of coverage you need.

Step 2: Use the OPM Comparison Tool

Once you have your information together, it's time to put it to work. The official OPM Plan Comparison Tool is your best friend during Open Season. This is an online resource that lets you compare plans side-by-side based on premiums, deductibles, out-of-pocket maximums, and other key features.

Just enter your zip code and pay system to see all the plans available in your area. You can filter them to see if your doctors are in-network and compare up to four plans at once. This tool is great for getting a high-level overview and helps you start narrowing down your choices from the 132 FEHB plan options available for 2026.

To help with your decision-making, exploring some Financial Wellness Apps and Platforms for Employee Benefits can also provide some useful tools to simplify the process.

Step 3: Dig Deeper into Plan Brochures

The OPM tool is fantastic for comparing plans, but the official plan brochure is where you confirm the details. Never make a final decision without reading the brochure for any plan you're seriously considering. The brochure is the legally binding contract between you and the insurance carrier.

Think of the OPM tool as the movie trailer and the plan brochure as the full film. The trailer gives you the exciting highlights, but the film has all the critical plot details and fine print you need to know before you commit.

Be sure to look for Section 5, "Benefits," to understand exactly what’s covered and what your cost-sharing will be for things like hospital stays, specialist visits, and prescription drugs.

Step 4: Submit Your Changes with Confidence

After you’ve done your homework and made a decision, the last step is to officially submit your changes. The specific portal you use depends on your agency, so double-check with your HR department if you're unsure. Most federal employees will use one of these systems:

- GRB Platform (Government Retirement & Benefits)

- Employee Express

- MyPay

- Employee Personal Page

Remember, if you’re happy with your current FEHB and FEDVIP plans, you don’t have to do a thing—they will automatically roll over. However, you must actively re-enroll in FSAFEDS every year if you want to participate. While you're at it, this is also a great time to review your life insurance needs. You can learn more about FEGLI changes during Open Season in our dedicated guide.

Real-Life Scenarios and Strategic Benefit Choices

Knowing the rules of the game is one thing, but seeing how decisions play out for real people makes it all click. Your own life—your family, your health, and your financial goals—is the single most important factor when choosing coverage during the open season federal benefits window.

Let's walk through a few common situations to see how different life stages call for completely different strategies. These stories help connect the dots between plan brochures and your everyday reality.

The New Hire Laying the Foundation

Meet Alex, a 27-year-old software developer just starting his federal career. He’s single, in great health, and his main goal is to stash away as much cash as possible for a down payment on a house. For him, a High-Deductible Health Plan (HDHP) paired with a Health Savings Account (HSA) is a fantastic fit.

Why? The HDHP comes with much lower premiums, leaving more money in his paycheck each month. But the real power move is the HSA. It gives him a triple-tax advantage: his contributions are tax-deductible, the money grows tax-free, and any withdrawals for qualified medical expenses are also tax-free.

Alex plans to use his HSA as a long-term investment vehicle. He knows he can use it to cover his deductible if something comes up, but his primary strategy is to let that money grow for decades. Every dollar he puts in now has the potential to become a substantial healthcare fund for retirement.

The Mid-Career Family Balancing Needs

Now, let's look at Maria, a 44-year-old manager with a spouse and two kids, ages 10 and 14. Her family’s needs are a lot more complicated. Her son’s travel soccer schedule brings the constant risk of sprains and breaks, and her daughter is definitely getting braces next year. While she's budget-conscious, what she really craves is predictability.

For Maria’s family, a traditional PPO plan is the clear winner. The premiums are higher, sure, but the low deductible and set copayments for doctor visits and prescriptions give her financial peace of mind. She knows exactly what a trip to urgent care will cost, which takes all the guesswork out of their monthly budget.

She also dove deep into the FEDVIP dental plans, specifically looking for solid orthodontic coverage. She chose a plan that covers 50% of the cost of braces up to a $2,500 lifetime maximum, a decision that will save her thousands. On top of that, Maria maxes out her Dependent Care FSA to pay for after-school programs with pre-tax dollars.

Your benefit strategy should be a direct reflection of your life's current chapter. A plan designed for saving on premiums may not serve a family that needs predictable access to care, and vice versa.

This is all about matching the right plan features to your specific, real-world needs.

The Pre-Retiree Securing the Future

Finally, there’s David, who is 61 and just four years away from retirement. His number one priority is locking in affordable, high-quality health coverage for the rest of his life. The choices he makes during these last few open seasons are absolutely critical.

David’s entire focus is on the FEHB “5-year rule.” He knows he must be enrolled in an FEHB plan for the five consecutive years before he retires to carry that coverage with him. The first thing he does is double-check his records to confirm his continuous enrollment, securing this priceless benefit.

With that confirmed, his attention shifts to picking a plan that will pair well with Medicare when he turns 65. He’s researching national PPO plans that either help reimburse Medicare Part B premiums or have excellent prescription drug coverage. He understands that making a smart choice now can drastically lower his healthcare spending in retirement.

He also recognizes that any big-ticket dental work—like a potential crown or implant—is best handled now, while he’s still earning his full salary. He opts for a high-option FEDVIP plan to get the best possible coverage and minimize his out-of-pocket costs before he transitions to a fixed income.

Each of these federal employees used the open season federal benefits period to perfectly align their coverage with where they are in life. By thinking strategically about their health, finances, and future, they made smart choices that deliver security and peace of mind.

When to Get Expert Guidance on Your Federal Benefits

Making the right choices during the federal benefits open season is empowering, but let's be honest—sometimes the sheer volume of information can feel like a heavy weight. While this guide gives you a solid foundation, some situations are just too complex to tackle alone. In those cases, calling in an expert is the smartest move you can make.

Think of it this way: you can probably handle changing your own oil, but you'd call a mechanic for a full engine rebuild. Your federal benefits are the engine of your financial security, and a small mistake now can lead to big, expensive problems down the road.

Key Moments to Seek Professional Advice

For many federal employees, navigating benefits year-to-year is pretty straightforward. But professional guidance becomes absolutely essential during major life transitions or when you're dealing with complicated health needs. A personalized review can uncover savings and strategies you would have never found on your own.

Consider reaching out for help if you find yourself in one of these situations:

- You're approaching retirement. The decisions you make in your final five years on the job, especially with your FEHB, can be permanent. There are no do-overs.

- You're going through a major life event. Things like marriage, divorce, or the birth of a child completely change your benefit needs and require careful, deliberate plan adjustments.

- You or a family member has a chronic health condition. Managing complex medical care or very expensive prescriptions requires a deep dive into plan details, drug formularies, and coverage limits that can be a full-time job in itself.

- You feel completely overwhelmed. If the options, acronyms, and rules just leave you feeling stuck and uncertain, a clear, expert opinion can provide immediate clarity and confidence.

A professional benefits review isn't admitting defeat; it's a strategic investment in your financial future. It's about making sure your benefits are perfectly aligned with your retirement goals and preventing costly errors before they happen.

A true expert can analyze your unique situation, run detailed plan comparisons based on your specific healthcare needs, and show you how your benefits strategy fits into your overall retirement plan. They translate the dense language of OPM brochures into actionable advice that fits your life.

If you're not sure where to begin, our guide on choosing the right employee benefits advisors can help you find the right fit. Don't let complexity lead to inaction; getting personalized support is a powerful step toward securing a stress-free retirement.

Your Top Open Season Questions, Answered

As the Open Season window starts to close, the same questions always seem to surface. It’s completely normal, and getting straight answers is the only way to make smart choices without second-guessing yourself later. Let's tackle four of the most common questions we hear from federal employees.

What Happens If I Miss the Open Season Deadline?

If you miss the deadline, your current FEHB and FEDVIP plans simply roll over for another year. That might sound like a relief, but it’s a passive decision that could cost you. You’re essentially accepting whatever new premium increases or coverage changes your plan has decided on for the next year.

The only way to change your core health, dental, or vision plans outside of Open Season is if you have a Qualifying Life Event (QLE). Think major life changes like getting married, having a baby, or your spouse losing their job and health coverage. Without a QLE, you're locked in until next year.

Can I Get FEDVIP if I'm Not in an FEHB Plan?

Yes, you absolutely can. This is a big point of confusion for many feds, but the Federal Employees Dental and Vision Insurance Program (FEDVIP) is a completely separate benefit. You don't need to be enrolled in a federal health plan to sign up for federal dental or vision coverage.

This gives you some valuable flexibility. For instance, maybe you get fantastic health coverage through your spouse's private-sector job, but their dental and vision plans aren't great. You can easily opt-out of FEHB and enroll only in FEDVIP to get the group rates.

How Does an HDHP with an HSA Actually Work?

A High-Deductible Health Plan (HDHP) combined with a Health Savings Account (HSA) is one of the most powerful tools in your benefits toolbox, but it’s often misunderstood. It’s really a two-part system: you have a health insurance plan that requires you to pay more out-of-pocket upfront (the high deductible), and in exchange, you get access to a special savings account.

The HSA is where the magic happens. It's a triple-tax-advantaged account, which is a huge deal.

- Tax-Deductible Contributions: Money you put in is pre-tax, which lowers your taxable income for the year.

- Tax-Free Growth: Your funds can be invested and grow over time, and you won't pay a dime of tax on the earnings.

- Tax-Free Withdrawals: You can pull money out for qualified medical expenses completely tax-free.

Unlike a "use-it-or-lose-it" FSA, the money in your HSA is yours forever. It rolls over year after year and can even be used as a supplemental retirement account down the road.

Do I Have to Re-Enroll in FSAFEDS Every Year?

Yes! If you only remember one thing about the Federal Flexible Spending Account Program (FSAFEDS), make it this: Your enrollment is not automatic. You must go in and actively re-enroll in your FSA every single Open Season.

Forgetting this is an easy and costly mistake. If you don't re-enroll, your contributions will stop, and you will not have an FSA for the next year. You'll miss out on a full year of tax savings on everything from co-pays to daycare expenses.

Making sense of all these rules to build a plan that truly works for you and your family can feel overwhelming. The experts at Federal Benefits Sherpa cut through the complexity to give you the clarity you need for a confident retirement. Schedule your free 15-minute benefits review today to make sure your benefits are perfectly aligned with your goals.